Warehousing in England (UK) - The New Post-Brexit Reality

Table of Contents

- The New Post-Brexit Reality – An In-Depth Guide for Logisticians and Shippers

- The Brexit Elephant in the Room: What has really changed for Warehousing in the UK?

- New Rules of the Game: The Most Important Provisions for Warehousing in England

- "Make or Buy"? The Strategic Decision: Self-Management vs. British 3PL Partner

- Practical Example: A German Medium-Sized Company and the 3PL Way

- ADSp? Attention contract traps! Tips for smooth implementation

- The Contract Logistics Company's view: Is it Worth having your Own Location in the UK?

- Global vs. Local: Warehousing in International Comparison (Focus Germany vs. UK)

- Dreams of the Future: Trends and Forecasts for UK Warehousing

- Conclusion

The New Post-Brexit Reality – An In-Depth Guide for Logisticians and Shippers

The British market was and is a central sales market for many companies from the EU. But since the UK left the EU Customs Union and the Single Market, logistics – and warehousing in particular – has become a strategic minefield. Simply sending a parcel across the channel no longer works smoothly. However, the demand for fast, reliable deliveries "as it used to be" has remained.

The logical consequence? A warehouse on site.

But what does this mean in practice? What hurdles have to be overcome, and which strategic decisions are essential for survival? Is it better to take the reins into your own hands (on your own) or to rely on an established British 3PL (Third-Party Logistics) partner?

This article dives deep into the matter, highlights the facts, compares strategies and gives practical tips for successful UK warehouse logistics in 2025.

The Brexit Elephant in the Room: What has really changed for Warehousing in the UK?

The biggest change is simple: the UK (United Kingdom) is a third country. Every movement of goods between the EU and the UK is now an import or export transaction. This has a massive impact on warehousing, far beyond pure transport.

- The customs border is real: Deliveries from an EU warehouse (e.g. Germany) to a UK customer (B2B or B2C) mean: export declaration (EU), import declaration (UK), potential customs payments and import VAT. This leads to delays and incalculable costs for the end customer.

- Value Added Tax (VAT) complexity: UK Value Added Tax (VAT) is a key issue. For shipments under £135, VAT often needs to be paid by the seller (i.e. the EU company) directly in the UK, which requires UK VAT registration. For higher values, the import VAT applies.

- Rules of Origin: Just because goods come from the EU does not automatically mean that they are duty-free. The Trade and Cooperation Agreement (TCA) between the EU and the UK only provides for duty-free status for goods that can prove a preferential EU or UK origin. Customs duties are incurred for goods that are imported into the EU from China, for example, and then resold unchanged to the UK (keyword: distribution center).

- The Border Target Operating Model (BTOM): The UK is gradually introducing the new "Border Target Operating Model" (since the end of 2023 and in the course of 2024/2025). This increases physical and documentary controls for many product groups (especially food, animal and plant products) and exacerbates the need for correct advance declarations.

A warehouse in the UK avoids the problem of individual customs clearance for each end customer order. Instead, the goods are imported once as bulk freight (e.g. an entire truck) and cleared through customs and can then be shipped from the UK warehouse as a "domestic delivery" to the end customer quickly and without customs hurdles.

New Rules of the Game: The Most Important Provisions for Warehousing in England

Anyone who wants to store goods in the UK or have them stored has to deal with a new regulatory thicket that does not exist in the EU single market.

Das "Fulfilment Houses Due Diligence Scheme" (FHDDS)

This is perhaps the most important, but often overlooked, regulation. Any company that stores goods in the UK that come from a seller based outside the UK (e.g. a German online shop) and are sold to private customers (B2C) must register with HMRC (the UK tax authority) for the FHDDS.

- What does that mean? The warehouse keeper (whether the German shop itself or a 3PL) is held accountable. He must carry out strict due diligence on his clients. He must ensure that his customer (the German shop) is correctly registered for VAT in the UK and also pays it.

- Risk: If he does not do this, the warehouse keeper may be liable for the customer's unpaid VAT. This makes collaboration riskier for 3PLs and more complicated for companies on their own.

Customs Warehousing

A bonded warehouse is a decisive strategic advantage. Goods can be imported into the UK without immediately incurring customs duties or import VAT.

- Advantage: Customs duties and VAT are only due when the goods are removed from the customs warehouse and released into free circulation in the UK (e.g. when sold to a customer). If the goods are re-exported from the customs warehouse, e.g. to the USA, there are no UK customs duties/VAT at all.

- Liquidity: This massively protects liquidity, as customs duties are not due when the entire truckload is imported, but only when the individual items are sold.

- Disadvantage: The establishment and operation of a customs warehouse (whether private or public) is subject to approval and requires complete inventory management and IT connection to customs (HMRC).

UKCA Marking

The UKCA mark (UK Conformity Assessed) replaces the EU CE mark for many products (e.g. machines, toys, electronics) for the UK market (England, Scotland, Wales). Goods that are in the UK warehouse and placed on the market there must bear this marking. (Note: The deadlines for this have been extended several times, but the changeover is unavoidable).

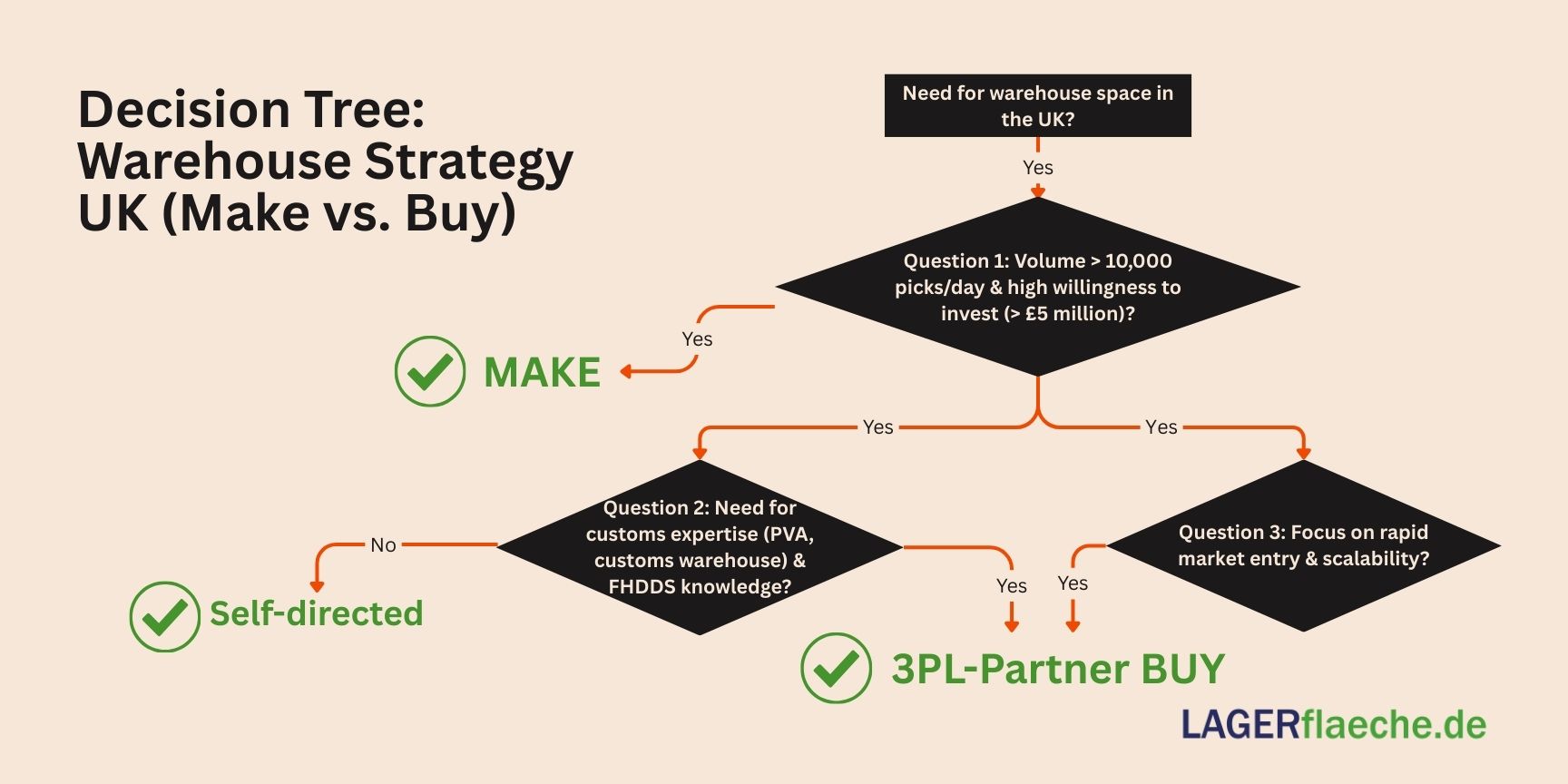

"Make or Buy"? The Strategic Decision: Self-Management vs. British 3PL Partner

The key question for an EU company is: Do I run a warehouse myself or do I hire a service provider?

Scenario 1: Self-management on behalf of the warehouse customer

Here, the EU company (or the "warehouse customer") rents a hall in England itself, hires staff and manages the processes.

- Pros:

- Full control over processes, quality and branding (e.g. packaging).

- Direct IT integration into your own systems (ERP, WMS).

- Potentially higher margin when volume is extremely high.

- Cons:

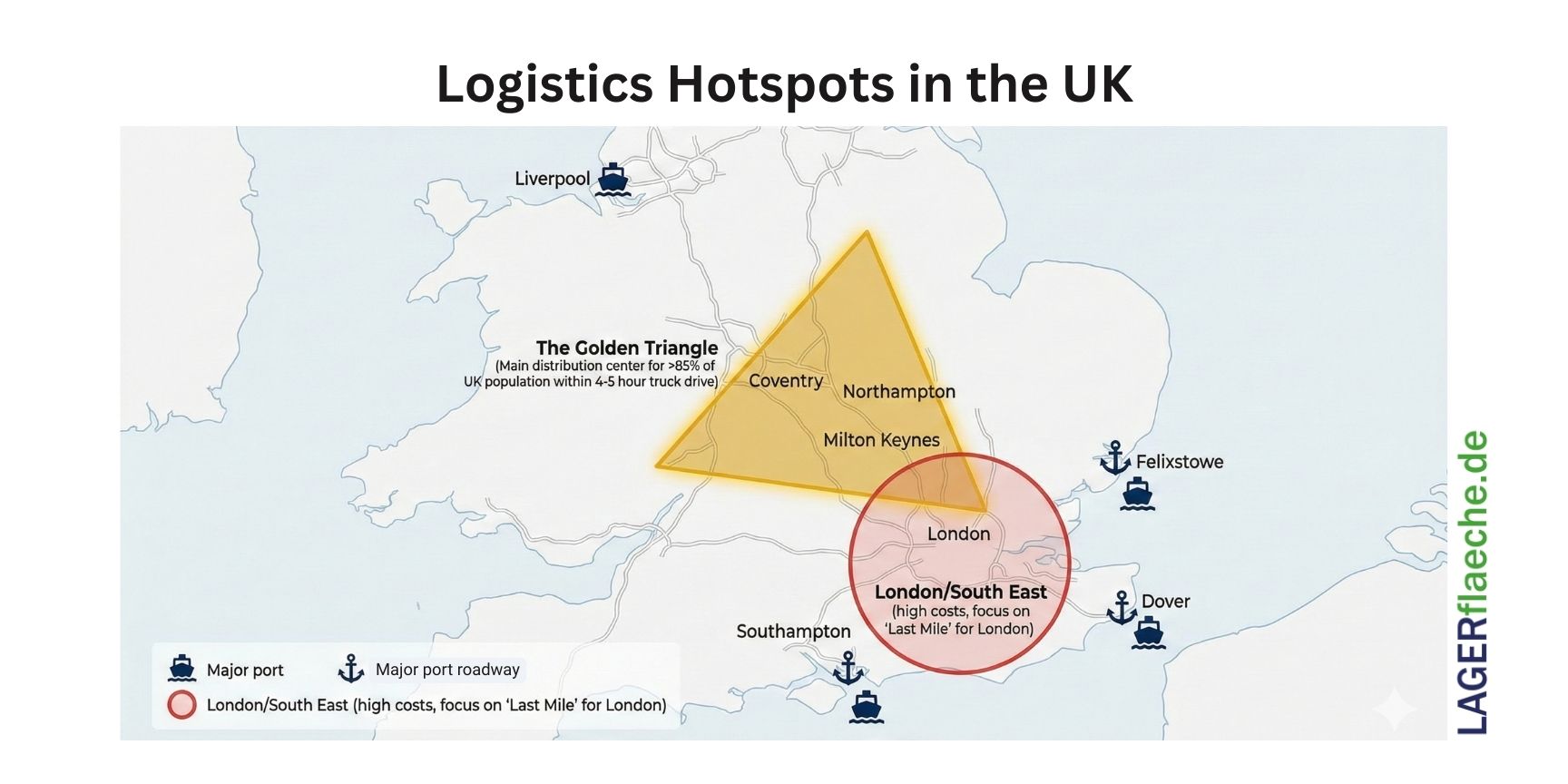

- Extremely high investment: The storage costs in the UK are exorbitant. According to the "Savills UK Warehouse Market Report" (Q1 2024), logistics space in the "Golden Triangle" (Midlands, around Northampton) is among the most expensive in Europe, with prime rents of over £10 per square foot.

- Staff shortage: The British labor market for logistics personnel (warehouse clerks, truck drivers) is extremely tight.

- Regulatory burden: The company has to take care of UK VAT, EORI number, FHDDS registration, customs software and potentially bonded warehouse licenses itself. An immense administrative effort in a foreign legal and tax system.

Scenario 2: Warehouse order to a British company (3PL)

The EU company uses a specialized contract logistics provider or fulfilment service provider in the UK.

- Pros:

- Expertise: The 3PL is familiar with the UK regulations (customs, VAT, FHDDS) and ideally already has a customs warehouse license (AEO status).

- Fast time to market: No time delay due to site search or staff recruitment.

- Scalability: The 3PL can cushion peaks (seasonal business).

- Risk minimization: The 3PL takes responsibility for compliance with many local regulations (occupational safety, warehousing).

- Cons:

- Dependence on the partner.

- Less control over the direct process and the "look & feel" at the customer.

- Cost: Good 3PLs with customs expertise are expensive.

- Data interfaces (IT connection) must be implemented cleanly.

Conclusion: For 95% of SMEs and even for many larger companies, the "buy" approach (3PL partners) is the much safer, faster and often more cost-efficient way to serve the UK market professionally after Brexit. The complexity of self-management has increased massively.

Practical Example: A German Medium-Sized Company and the 3PL Way

"Präzisionsteile Müller GmbH" from Germany sells high-quality tool components (B2B) and special tools (B2C) via its online shop. Before Brexit, the UK was a top 3 market.

- Problem (early 2021): After Brexit, B2C sales collapsed. Customers complained about unexpected customs fees and weeks-long delivery times. B2B customers (British factories) were in danger of bailing out because they could no longer get their spare parts "Next Day".

- Analysis: The single mailing was dead. A solution on site was necessary. The self-management was rejected due to the complexity of the FHDDS, the unclear VAT location and the high investment in a small warehouse.

- Solution (implementation in 2022): Müller GmbH selected a 3PL partner in the "Golden Triangle" (close to the M1 motorway for fast distribution).

- VAT/EORI: Müller GmbH registered for a UK VAT number and a UK EORI number.

- 3PL selection: The partner was AEO (Authorised Economic Operator) certified, FHDDS registered and offered a bonded warehouse (Type A, Public).

- Process: Müller GmbH now sends a collective shipment (pallets) by truck to the UK warehouse every 2 weeks.

- Customs clearance: The 3PL takes care of import customs clearance as a "direct representative". Import VAT is only recorded on the balance sheet via Müller GmbH's "Postponed VAT Accounting" (PVA) and is not paid at the border (massive liquidity advantage). Customs duties (for goods of non-EU origin) are only due when they are removed from the customs warehouse.

- Fulfilment: B2C and B2B orders from the German shop are transferred to the WMS of the 3PL via API. This picks, packs and ships via Royal Mail or DPD (UK) – with delivery on the next day.

- The result: customer satisfaction is back to pre-Brexit levels. Costs have increased due to the 3PL fees, but they can be planned and are more than compensated for by the volume of sales held (and even growing).

ADSp? Attention contract traps! Tips for smooth implementation

Anyone doing business in Germany is used to the ADSp (General German Freight Forwarders' Conditions). They clearly regulate liability and obligations.

This standard does not apply in the UK!

- UKWA Conditions: Many (but not all) UK warehousekeepers and 3PLs operate on the basis of the UKWA (UK Warehousing Association) Conditions.

- The crux of the matter: These conditions are extremely advantageous for the warehouse holder, especially in terms of adhesion. The liability limits are often very low and the exclusions of liability are far-reaching.

- Tip: Never rely on German standards. The contract with the 3PL must be legally reviewed (ideally by a lawyer with UK expertise). In particular, the liability sums must be negotiated and the insurance cover (goods insurance) must be adjusted!

More quick tips for success:

- Master data is gold: The basis for every customs declaration is correct data. Commodity codes (HS codes), country of origin and value must be maintained in the ERP system for each individual item. Without this, bulk imports will fail.

- IT integration: The interface (API, EDI) between your ERP and the WMS of the 3PL partner is the heart of it. There must be no savings here.

- Choose the right 3PL: Don't look for the cheapest, but the most competent. Ask specifically about: AEO status? FHDDS Registration? Experience with PVA? Experience with your industry?

The Contract Logistics Company's view: Is it Worth having your Own Location in the UK?

What if we (as a German logistics service provider) follow our customers and open a warehouse in England ourselves?

This "make" decision on the service provider side is a strategic bet in the double-digit million range.

- The opportunity: The market for competent 3PLs is huge. Many EU companies are desperately looking for partners who can build the EU-UK bridge for them. Anyone who offers AEO, bonded warehouses and FHDDS compliance from a single source has a strong selling point.

- The challenges (facts):

- Real estate costs: As mentioned, rents are extremely high. According to Savills (Q1 2024), the vacancy rate in the UK logistics sector was only around 4-5% – a clear landlord market.

- Workforce: The shortage of skilled workers and workers (post-Brexit migration effects) is a chronic problem. Wages in the logistics sector have risen sharply.

- Compliance investment: You need your own, highly qualified customs personnel, expensive software licenses for the customs connection (e.g. to the "Customs Declaration Service" - CDS) and have to pass the strict audits for AEO and customs warehouse licenses.

- The "Windsor Framework": Northern Ireland (NI) is a special case. Through the Windsor Framework, NI remains virtually in the EU internal market for goods. Deliveries from the EU to NI are (simplified) like domestic movements, deliveries from GB to NI require customs declarations. A warehouse in NI could be strategically interesting, but it serves a different market than a warehouse in England.

Conclusion: Having your own location is a high-risk/high-reward scenario. It only makes sense for large, well-funded contract logistics companies that already have a clear customer base to accompany them to the UK and are willing to overcome the high barriers to market entry.

Global vs. Local: Warehousing in International Comparison (Focus Germany vs. UK)

Why is warehousing in the UK so different from that in Germany or other countries?

UK vs. Germany (as EU member):

- Core difference: customs border vs. internal market. In Germany, a warehouse in Hamburg can easily serve customers in Munich or Milan (Italy) without customs involvement (goods are in free circulation).

- Regulation: In Germany/EU, the Union Customs Code (UCC) regulates customs warehouses. In the UK, it is British national law (HMRC).

- Standards: In Germany, ADSp are a quasi-standard. In the UK (as described above), a different, more warehouse-friendly standard prevails with the UKWA conditions.

- Market: The German market is geographically more central for EU distribution. The UK market is an "island" (literally and regulatory).

UK vs. USA:

- Complexity: The U.S. does not have a customs border within the country, but it does have a massive complexity due to the states. A warehouse in New Jersey must calculate sales tax differently for deliveries to California than for deliveries to Texas. The U.S. is 50 different tax systems.

- Size: The sheer geographic size of the U.S. often requires multiple warehouse locations (e.g., East Coast, West Coast, Midwest) to ensure nationwide 2-day deliveries. In the compact UK, a central location (e.g. Midlands) is often sufficient.

UK vs. China (Asia):

- State influence: In China, logistics is strongly controlled by state planning and Free Trade Zones (FTZs). The regulatory requirements are high and often opaque.

- Technology: Asia, especially China and Japan, is a leader in warehouse automation and robotics (e.g. Cainiao, Alibaba).

- Purpose: Warehouses in China (e.g. Shanghai FTZ) often serve as global production and export hubs, while a warehouse in the UK is primarily a distribution hub for the local UK market.

Why the differences? They are based on political geography (EU single market vs. third country UK vs. federal USA), trade policy (TCA, NAFTA/USMCA) and legal traditions (civil law in Germany vs. common law in the UK/USA).

Dreams of the Future: Trends and Forecasts for UK Warehousing

How will the situation develop? Setting up a warehouse in the UK is a long-term decision.

- Digital border: The UK is driving forward the digitization of the border. The "Single Trade Window" (STW), which is to be fully implemented by 2027, aims to bundle all import/export data in a single digital place. This could simplify bureaucracy in the long term – but only for those whose master data and IT systems are ready for it.

- Automation as a constraint: The combination of high labor costs and labor shortages will accelerate automation in UK warehouses. Robotics (AMRs) and "goods-to-person" systems are going from "nice-to-have" to "must-have" to achieve competitive pick costs.

- Stabilization: The "shock phase" of Brexit is over. The processes (PVA, bonded warehouses) are stabilizing. Companies that master the complexity now secure a lasting competitive advantage over those that avoid the UK.

- The 3PL dominance: The trend will clearly move away from self-management and towards specialized 3PLs. The regulatory barrier to entry (FHDDS, customs) is too high for most shippers to handle alone.

Conclusion

Warehousing in England has undeniably become more complex and expensive as a result of Brexit. However, it is also the only way to continue to serve the demanding UK market with the speed and reliability that customers expect.

The question is no longer whether, but how.

For almost all EU companies, the strategically smartest path is through an experienced British 3PL partner who can shoulder the regulatory burdens (especially customs, VAT and FHDDS). Self-management remains a risky undertaking for financially strong large companies.

Success in post-Brexit trade is no longer determined solely by the product, but by the quality, efficiency and compliance of the underlying logistics chain.

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....

The Hidden Costs of Poor Contract Logistics: Where Is Your Margin Bleeding?

Stop losing your margin: Uncover the hidden cost traps in your contract logistics and optimize your supply chain....

Logistics Real Estate of the Future: Are We Building Down Instead of Out?

A shortage of space and skyrocketing land prices are forcing the logistics industry to rethink its approach—is building underground the solution? Find out in our in-depth expert analysis what enormous potential fully automated “dark warehouses” and urban micro-hubs hold for the future of the industry....