The New Power of Platforms: How Amazon, Temu and Shein Rewrite the DNA of Logistics

Table of Contents

- The Strategic Shift: From Air Freight Parcel to Local Warehouse

- The "Amazonization" of Chinese Players: An Infrastructure Comparison

- The Power Dilemma: When the Customer becomes a Competitor

- Europe in comparison: Germany vs. the rest of the world

- The Elephant in the Room: Customs Clearance and the 150 euro limit

- Returns Management: The Sore Point of Cheap Logistics

- Case Study: How a Medium-Sized Logistics Company has to React

- Conclusion and Outlook: The Survival Formula for Europe's Logistics

- Tabular Overview: Logistics Models in Comparison

Is your logistics network ready for the "China Speed"? Or are you still relying on strategies from the last decade?

Global trade is in one of the most radical phases of upheaval in its history. It is no longer just the battle for the customer that is being fought online – it is a battle for sovereignty over the physical infrastructure. While we talked about "just-in-time" for years, players like Amazon, but especially the new Chinese giants Temu, Shein and TikTok Shop, are pushing a new era: "Direct-to-Consumer at Hyper-Speed".

The days when Chinese goods bobbed on a container ship for weeks are over. With massive investments in their own fulfillment and distribution centers in Europe, these platforms are sawing at the chairs of established logistics service providers and forcing the entire market to rethink.

In this deep dive, we analyze how retail structures are shifting, why Germany plays a special role in this and what strategic answers logistics companies and retailers must now find.

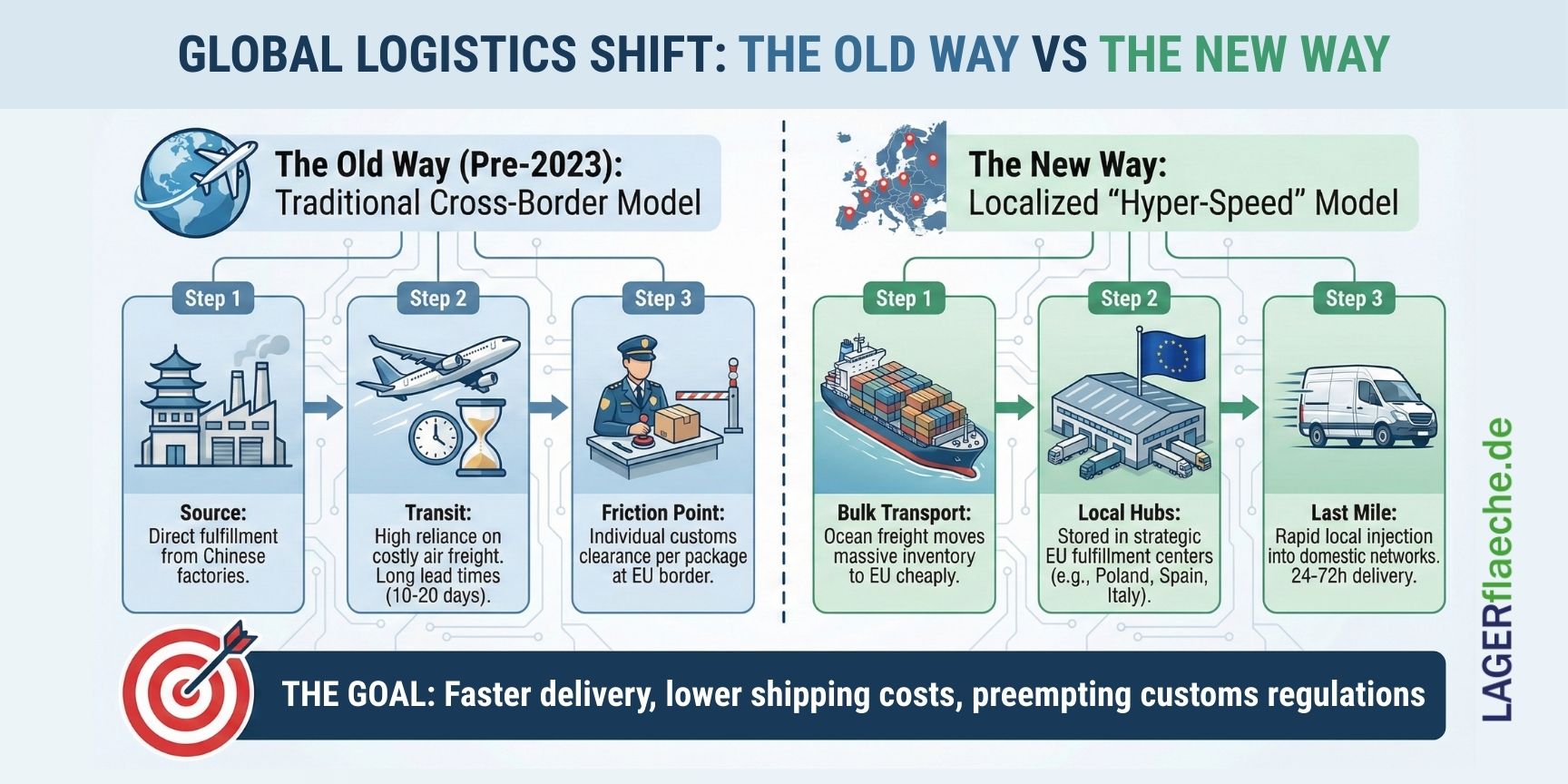

The Strategic Shift: From Air Freight Parcel to Local Warehouse

For a long time, Shein and Temu's business model was based almost exclusively on direct air shipping from China (cross-border). But this model is reaching its limits: rising air freight rates, stricter customs controls and the call for sustainability. The response of the giants? They become local.

Why the platforms are suddenly becoming sedentary

The goal is clearly defined: faster delivery times, lower shipping costs, efficient customs clearance and local returns management. If you want to deliver within 24 to 48 hours, you can't ship from Guangzhou.

- Temu: Now operates warehouse locations and partnerships in Germany, France, Spain, Italy, the Netherlands and Austria.

- Shein: Has established strategic centers in Belgium, Frankfurt (Germany), Spain, Italy, Ireland, and Poland .

- Amazon: Invented this game and has been perfecting its network in Germany and Europe for years.

Important question: Why are asset-light platforms like Temu suddenly investing in asset-heavy structures?

The answer: It's about risk minimization. By storing locally, they avoid potential bottlenecks in air freight and anticipate upcoming EU regulations (such as the abolition of the 150-euro duty-free limit). In addition, local availability massively increases the conversion rate.

The "Amazonization" of Chinese Players: An Infrastructure Comparison

It is worthwhile to look at the networks in detail to understand the force of the change.

The Amazon model as a blueprint

Amazon has an extremely close-knit network of fulfillment centers (FCs) and distribution centers (delivery stations) in Germany. The strategy: bring the goods as close as possible to the customer in order to enable "same-day delivery". Amazon often acts as a logistics provider itself (Amazon Logistics) and displaces classic parcel services.

Shein and Temu's race to catch up

While Amazon controls the "last mile" itself, Temu and Shein focus on the "middle mile" and warehousing.

- Shein in Poland: Poland often serves as the "backend" for the German market. Large warehouses near the German border enable fast deliveries without the high German labor and location costs.

- Temu in Southern Europe: The expansion in Italy and Spain aims to serve markets that are often more logistically fragmented than the DACH region.

Graphic suggestion (description): A map of Europe that marks the warehouse locations of Amazon (blue), Shein (red) and Temu (orange). Cluster formation in Eastern Europe (Poland/Czech Republic) should be particularly striking as a supply hub for Western Europe. (Source of the database: Analysis of industry reports such as Logistik Heute or DVZ, 2023/2024).

The Power Dilemma: When the Customer becomes a Competitor

A central problem for traditional logistics service providers (3PLs) and parcel services (CEP) is the enormous market power of these platforms.

The loss of bargaining power

If a significant part of the global shipment volumes is controlled by a few players, they dictate the prices.

- Volume trap: A logistics company that generates 30% of its volume through Temu parcels alone is susceptible to blackmail. If Temu threatens to change, the business collapses.

- Seasonal peaks: The platforms create artificial peaks (e.g. "Temu Week") that exceed the capacities of the service providers, but do not offer long-term planning security.

Fact check: The air freight volume

According to reports from Reuters and Cargo Facts, Shein and Temu claimed over 30% of daily air freight capacity from southern China at times in 2023 . This drove up prices for all other market participants and narrowed the space for classic B2B shipments.

Europe in comparison: Germany vs. the rest of the world

Logistics structures do not change in the same way everywhere. There are massive differences driven by geography, labor costs, and regulation.

Germany: The Expensive Giant

Germany is the largest e-commerce market in Europe, but also one of the most expensive and complicated for logistics companies.

- Challenge: High wage costs, strict labour laws (Verdi), expensive land prices and bureaucratic hurdles for building permits.

- As a consequence, platforms use Germany as a sales market, but are increasingly relocating warehouse logistics to the surrounding area.

Poland & Czech Republic: The workbench of e-logistics

Compared to Germany, Poland and the Czech Republic have become the true logistics hubs.

- Advantages: Significantly lower labour costs, flexible labour markets, fast approval procedures and geographical proximity to German conurbations (Berlin, Dresden, Leipzig).

- Shein's strategy: The distribution center in Wrocław serves the German market. The goods are "felt" in Germany, but in Poland for tax and operational purposes.

USA vs. Europa

In the US, Chinese platforms often exploit the "de minimis" rule (duty-free under USD 800) even more aggressively than in Europe (EUR 150). In addition, they are establishing their own "last mile" partnerships with local courier services in the USA to bypass USPS and UPS. In Europe, people are more dependent on the national postal companies (DHL, La Poste), but try to push them down in price by bundling volumes.

The Elephant in the Room: Customs Clearance and the 150 euro limit

A major driver for the establishment of local warehouses is the threat of a change in customs policy.

Interesting question: What happens if the EU overturns the duty-free limit of 150 euros?

Currently, Shein and Temu benefit massively from the fact that shipments under 150 euros can be imported duty-free into the EU (only import sales tax is incurred, often handled via the IOSS procedure). However, the EU Commission is planning a customs reform that could abolish this border.

The strategic answer: If Chinese goods suddenly have to be cleared through customs, direct shipping from China will become more expensive and slower (bureaucracy). Local camps in the EU are the insurance against this reform. If the goods have already been imported duty-paid in a warehouse in Spain or Poland (bulk import), the customer's individual order no longer plays a role in customs law. This guarantees "Frictionless Trade".

Returns Management: The Sore Point of Cheap Logistics

Until now, the motto has often been: "Just keep it, it's not worth sending it back." But with rising prices and the desire for higher customer loyalty, this is changing.

Local consolidation

Temu and Shein are increasingly working with local service providers to bundle returns. Instead of sending each package back to China (economic madness), the goods will:

- Tested in local centers (e.g. in Italy or Poland).

- Resold as B-stock to local buyers (liquidation).

- Or annihilated (which is increasingly encountering regulatory resistance).

Pressure to innovate: This creates a market for specialized "reverse logistics" providers who can efficiently process these huge quantities without having to return to Asia.

Case Study: How a Medium-Sized Logistics Company has to React

Let's look at a fictitious but realistic scenario: "Müller Logistics GmbH" from North Rhine-Westphalia.

Initial situation: Müller Logistics made 40% of its sales through fulfillment for Amazon merchants (FBA alternatives) and imports from Asia. Suddenly, they lose customers because they switch directly to Shein's cheaper fulfillment services or Amazon makes the fees for its own logistics so attractive that external service providers are excluded.

Strategic action (the solution):

- Diversification: Müller must no longer rely only on "Big Tech". The focus must be on niche customers (e.g. medical technology, high-quality furniture) who have special requirements that Temu/Amazon cannot offer "off the shelf".

- Partnerships with rules of the game: If Müller works for Temu (e.g. as a local hub), then only with contractually fixed minimum volumes and price clauses that protect against sudden fluctuations.

- Technology offensive: Integration of AI to predict order volumes to plan personnel more efficiently than the large, rigid networks.

- Finishing: Offering value-added services (e.g. fashion ironing service, personalization) that are not possible in the giants' mass warehouses.

Conclusion and Outlook: The Survival Formula for Europe's Logistics

The transformation through Chinese and American platforms is not a temporary trend, but a structural realignment of global trade. The pressure on delivery times and costs will continue to increase.

Die Key Takeaways:

- Localization is mandatory: If you want to sell in Europe, you have to store physically in Europe.

- Data sovereignty decides: Whoever has the data on inventories and customer flows controls the chain.

- Germany must become more efficient: In order not only to be a sales market, but also to remain a logistics location, automation and flexibility must compensate for the high costs.

For logistics service providers, this means that specialisation beats mass. Anyone who tries to undercut Temu in price will lose. But those who solve the complexity that causes the giants' algorithms to fail (bulky goods, dangerous goods, white-glove service) have a golden future.

Question for you: Have you already checked your supply chain for diversification, or are you dependent on a single big player?

Tabular Overview: Logistics Models in Comparison

| Feature | Classic online trading | Amazon FBA | Temu / Shein |

| Warehouse location | Decentralised / National | Network across the EU | Mix: China (Luft) + Hubs in PL/IT/ES |

| Delivery period | 2-4 days | 1 Day / Same Day | 5-9 Roofs (Air) / 2-4 Roofs (Local) |

| Customs | Import by dealer | Import by dealer | IOSS (Customer) or Bulk Import (Platform) |

| Focus | Brand & Service | Velocity | Preis & Gamification |

| Last Mile | DHL, Hermes, DPD | Amazon Logistics + Partner | Local partners (often the cheapest) |

(Note: The location data mentioned is based on the companies' expansion strategy as of 2023/2024. Sources for more in-depth research: Handelsblatt, Logistik Heute, DVZ - Deutsche Verkehrs-Zeitung, quarterly reports from Amazon and PDD Holdings).

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....

The Hidden Costs of Poor Contract Logistics: Where Is Your Margin Bleeding?

Stop losing your margin: Uncover the hidden cost traps in your contract logistics and optimize your supply chain....

Logistics Real Estate of the Future: Are We Building Down Instead of Out?

A shortage of space and skyrocketing land prices are forcing the logistics industry to rethink its approach—is building underground the solution? Find out in our in-depth expert analysis what enormous potential fully automated “dark warehouses” and urban micro-hubs hold for the future of the industry....