REALOGIS: Large-scale deals led to a significant increase in take-up in Munich's logistics and industrial real estate market in 2025

- Take-up increased by 39% to 320,000 m²

- Prime rent climbed to a new high of €13.50/m²

- Retail was the largest user group with 115,900 m²

- Existing space dominated the market

- Areas from 10,001 m² with 133,400 m² are the largest size class in terms of take-up

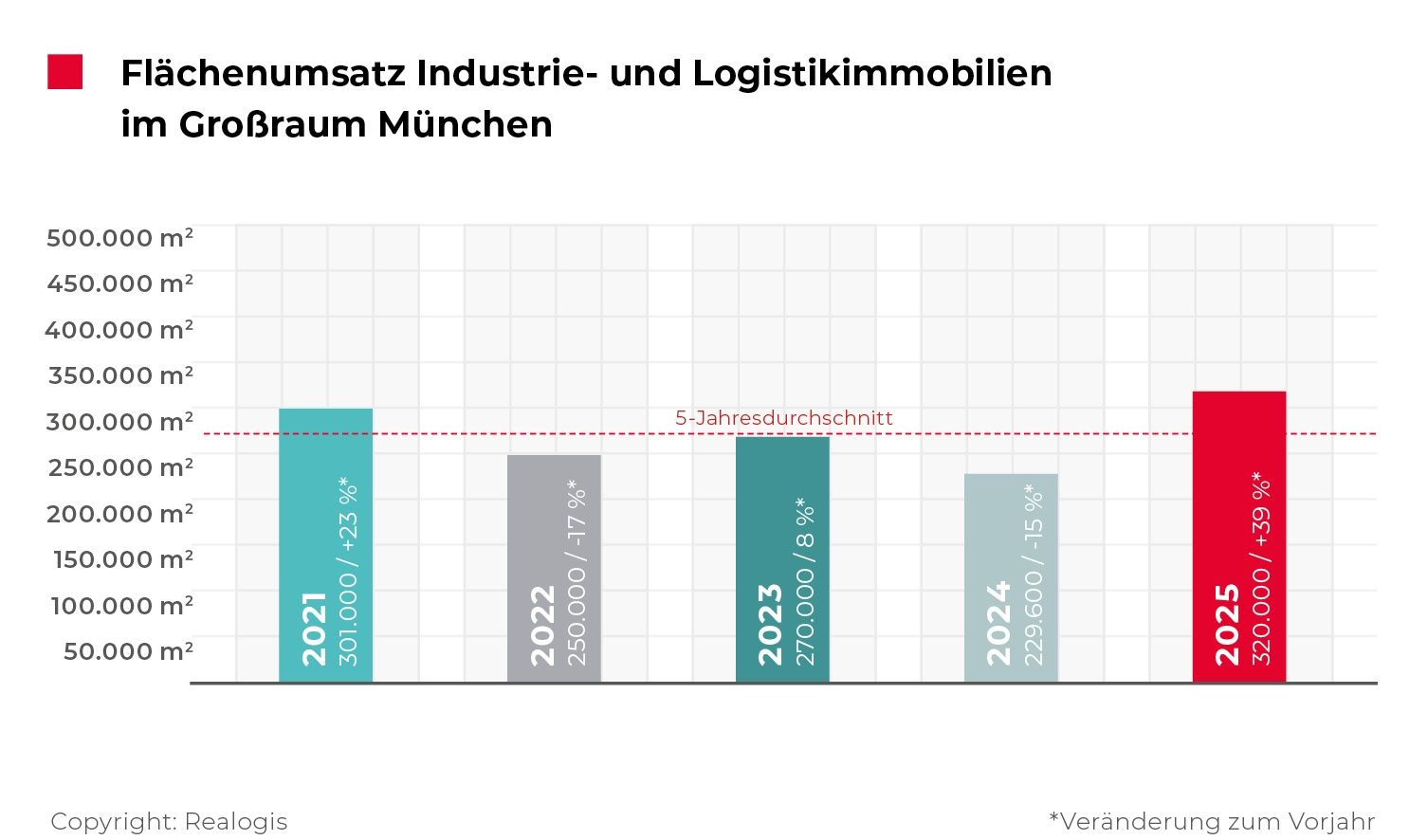

Munich, 23 January 2026 – The REALOGIS Group, Germany's leading consulting firm for industrial and logistics properties as well as commercial properties, registered take-up of 320,000 m² in the logistics and industrial real estate tenant market in Munich as a whole in 2025. Compared to the previous year, this corresponds to an increase of 90,400 m² or 39% (2024: 229,600 m²). The 5-year average was exceeded by 17%. The main revenue drivers were TTI, REPA, Sonima, Rohlik and Agile Robots. Together, they contributed 108,300 m² or 34% of total take-up.

Nicolas Werner, Managing Director of REALOGIS Immobilien München GmbH, explains: "2025 was one of the strongest years because companies in Munich and the surrounding area continue to be very robustly positioned. Demand for space remains correspondingly high, while supply is not keeping pace. There is no short-term relief in sight."

Rents: Peak value rises significantly, average rent rises moderately

Prime rents rose by 23% year-on-year to a new high of €13.50/m² (2024: €11.00/m²), continuing the upward trend since 2022. The average rent rose by 6% to currently €9.00/m² (2024: €8.50/m²). Prime and average rents reached their current peak at the end of the 1st half of 2025 and have been stable since then.

Spitzenmieten_1.jpg)

Take-up: Stock dominates, brownfields are back

Leases in existing properties dominated the market in 2025, reaching 199,000 m² or 62% of total take-up (2024: 111,400 m² / 49%). Two major deals by Rohlik and Agile Robots contributed 12% to the result. New greenfield buildings ranked second with 77,500 m² or 24% (2024: 118,200 m² / 51%). The major deals by TTI (35,700 m²) and Sonima (17,000 m²) account for 68% of the segment's turnover.

After no deals were registered on former brownfields in the past three reporting periods, they played a role again in 2025 and reached 43,500 m² or 14%. The major deal by REPA contributed around 75% to the segment result at 32,600 m². Munich remained a pure rental market in 2025 as a whole,

Types of buildings: "Other" are growing strongly, big-box space is losing market share

With regard to the type of building, in 2025 there were in particular deals in properties that could not be assigned to the category of big-box space or a business park structure. This collective category accounted for 184,400 m² or 57% of the space leased.

Big box space remained in second place with 82,400 m² or 26% of the share of space taken up (2024: 95,400 m² / 43%). They are the only type of building to miss their previous year's value. Business park leases once again occupy third place with 53,200 m² or 17% (2024: 34,300 m² / 15%).

Regions: North remains in the lead, west with strongest growth

The North region further expanded its leading position, reaching 168,200 m² or 53% share of take-up (2024: 108,200 m² / 47%). The 5-year average of 140,020 m² was exceeded by 20%. The major deals by REPA (32,600 m²) and Sonima (17,000 m²) contributed 29% to the region's take-up.

The West region, which had previously been in third place, followed in second place with 81,600 m² or 26% (2024: 24,200 m² / 11%). This is where the most significant growth was recorded, resulting in a result well above the 5-year average of 55,500 m2. The two deals by TTI (35,700 m²) and Agile Robots (10,200 m²) accounted for 56% of total take-up here.

The eastern region was the only one to suffer losses in take-up in third place. 52,700 m² or 16% of take-up was registered here (2024: 83,800 m² / 36%). The major deal by Rohlik (12,800 m²) was responsible for 24% of sales.

The South region continues to rank in the bottom with 17,500 m² and a share of 5% (2024: 13,400 m² / 6%), although the rented area increased by 4,100 m² or 31%.

Industries: Retail leads, e-commerce collapses

The strongest sector in 2025 as a whole was retail with 115,900 m² or 36% market share (2024: 78,500 m² / 34%), replacing the industry/production sector in the top position. Within retail, traditional retail dominates with 103,100 m² or 89% (2024: 30,100 m² / 38%). The two largest deals, TTI (35,700 m²) and REPA (32,600 m²), account for 66% of take-up in traditional retail. E-commerce is collapsing significantly: at 12,800 m², Rohlik's major deal is the only lease in the industry. Take-up was thus only about a quarter of the previous year's figure (2024: 48,400 m² / 62%).

Logistics/freight forwarding follows in second place with 104,500 m² or 33% (2024: 48,700 m² / 21%). With an increase of 115%, this corresponds to the most significant growth of all industries. Industry/production ranks third with 88,500 m² or 28% (2024: 81,100 m² / 36%) and recorded moderate growth of 7,400 m². The "Other" category was the only one to record a decline in the numbers and remained subordinate at 11,100 m² or 3% (2024: 21,300 m² / 9%).

Size classes: Large areas remain in the lead, areas between 5,001 and 10,000 m² are catching up

Large spaces of 10,001 m² or more remained the frontrunners with 133,400 m² or 42% market share (2024: 128,900 m² / 56%). The 5-year average of 104,020 m² is exceeded by 28%. Spaces between 5,001 m² and 10,000 m² rank second with 66,400 m² or 21% (2024: 23,900 m² / 10%). They exceed their 5-year average of 53,120 m² by a quarter (25%).

Medium to larger areas between 3,001 m² and 5,000 m² climb to third place with 52,700 m² or 16% (2024: 17,100 m² / 7%). Smaller areas between 1,000 m² and 3,000 m² slip to fourth place and reach 48,600 m² or 15% share (2024: 49,400 m² / 23%). They are the only size class to miss their 5-year average by 27%. Very small areas of less than 1,000 m² will remain subordinate, but will increase to 18,900 m² or 6% (2024: 10,300 m² / 4%).

Key figures at a glance

- Take-up: 320,000 m²

- Prime rent: €13.50/m²

- Average rent: €9.00/m²

- Existing areas: 199,000 m² | New building on a greenfield site: 77,500 m² |

New building on brownfield: 43,500 m²

- Tenants: 320,000 m² | Owner-occupier: 0 m²

REALOGIS. The No. 1 in industrial and logistics real estate

The REALOGIS Group is Germany's leading address for advising and brokering industrial and logistics properties as well as commercial properties. As an owner-managed company with locations in Berlin, Düsseldorf, Germany South/North, Frankfurt am Main, Hamburg, Leipzig, Munich and Stuttgart, the company, founded in 2005, has in-depth market knowledge and more than twenty years of experience in the German real estate sector.

Around 70 employees support national and international companies from logistics, industry, trade and e-commerce as well as private and institutional investors. The range of services includes the mediation of tenants for existing and new properties, the support of investors in acquisitions and project developments, advice on the search for or sale of land as well as the development and implementation of holistic real estate strategies, from location analysis to the realisation of assets that are no longer necessary for operation.

Contact Media

Targa Communications

Arne Degener

T +49 151 196 933 90

E ad@targacommunications.de

Latest Warehouse News

Topping-out ceremony for Panattoni Park Lübeck Süd: New location with international prospects

The modern logistics and production site with a total area of around 46,000 m² is located in the newly developed Semiramis industrial park, one of the last large industrial areas in the Hanseatic city...

The Evolution of Commerce, the "Slow Rise" of AI, and Hyper-Personalization: Supply Chain and Retail Predictions for 2026

Technological advancements remain rapid, global dynamics are changing almost daily, and consumer expectations are changing faster than at any time in retail history...

Successful completion: Panattoni sells innovative multi-tenant project in Berlin to DWS

The fully let Panattoni Campus Berlin Zentrum has been successfully sold to DWS Group, a leading asset manager in Europe with a global reach....

Panattoni realises modern bakery for Edeka Südwest

Edeka Südwest will rely on a new, state-of-the-art production site for this purpose in the future...