Logistics letting market awaits better economic prospects

Space take-up in Munich increases significantly, Hamburg slumps by a third

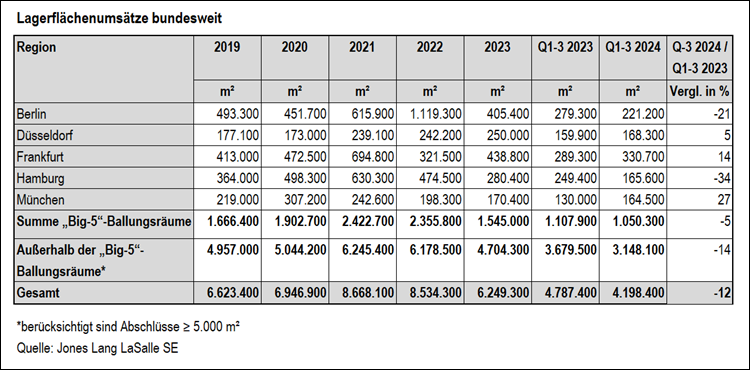

FRANKFURT, 4 November 2024 - Even after the first nine months of 2024, the German market for warehouse and logistics space is unable to match the previous year's figures. Around 4.2 million m² have been taken up since the beginning of the year, 1.08 million m² of which was by owner-occupiers. This was not only twelve per cent below the previous year's figure, but also the weakest result in nine months since 2014 (4.0 million m²). The five-year average was missed by 25 per cent and the ten-year equivalent by 19 per cent. At 510 contracts, the number of contracts signed has only fallen by four per cent since the previous year, but in a five-year comparison, the decline amounts to 15 per cent.

"Tenants and owner-occupiers are currently receiving many different signals that are making it difficult for them to make decisions," says Sarina Schekahn, Head of Industrial & Logistics Agency JLL Germany. "While numerous economic and sector outlooks show little movement or are more negative than hoped, inflation is following a downward trend despite individual fluctuations and the European Central Bank is lowering its key interest rate. However, demand for logistics space is likely to remain at the current low level. We currently anticipate take-up of around 1.5 million m² for the fourth quarter and thus 5.7 million m² for the year as a whole. It is highly unlikely that the previous year's figure of 6.25 million m² will be reached."

Mixed developments in the five metropolitan areas

In the so-called "Big 5" (Berlin, Düsseldorf, Frankfurt, Hamburg and Munich), around 1.05 million m² was taken up in the first nine months, which is only five per cent less than in the same period last year. However, at minus 31 per cent compared to the five-year average, take-up fell much more sharply.

The developments in the individual markets differ significantly: Frankfurt was once again the strongest region in terms of take-up with 330,700 m², which corresponds to an increase of 14 per cent. At 27 per cent, the increase was even greater in Munich, where 164,500 m² was taken up, the largest take-up of the five regions: Owner-occupier Group 7 began construction of its 60,000 m² logistics centre in Oberding in the first quarter. The Munich region also accounted for the largest transaction in the third quarter - a letting of around 28,000 m² by an industrial company in Vaterstetten. Düsseldorf also recorded at least a slight increase of five per cent, where 168,300 m² was taken up. The remaining regions paint a completely different picture: While Hamburg, with 165,600 m², suffered a significant drop of 34 per cent, Berlin also fell far short of the previous year's figure with 221,200 m² and minus 21 per cent.

Similar differences can be seen in demand: the largest share of take-up was accounted for by companies from the industrial sector with 330,100 m², closely followed by transport, traffic and warehousing with 323,100 m² - while the former increased their share by ten per cent, the latter fell by 26 per cent. Retail companies recorded a slight increase of four per cent with 229,800 m².

"Although the metropolitan areas are still in high demand among warehouse and logistics users, there is still a certain degree of caution when making large-scale property decisions," says Schekahn. "The majority of tenants and owner-occupiers still want to realise their plans, although some are postponing them until next year or the years after. Interim solutions such as lease extensions, subletting or additional lettings of smaller spaces are the consequence. Accordingly, the shifts in the order of magnitude of more than 10,000 m² are clear, where the number of agreements has declined."

This category accounted for 19 contracts totalling 336,100 m² in the first nine months, six deals and 25 per cent less space than in the same period of the previous year. The trend is even clearer in a five-year comparison with 14 agreements and 46 per cent less space. The 2,500 m² to 10,000 m² segment is much more in demand, accounting for 45 per cent of take-up and thus 17 per cent more than in the same period last year.

Completions are falling, prime rents are only rising in Berlin

There was also a significant decline in completions of new warehouse space: Only around 240,000 m² were finalised, around half as much as in the same period of the previous year and around 56 percent less than the five-year average. Around two thirds of the space had already been let or allocated to owner-occupiers before completion. At the end of September, around 490,000 m² was under construction, of which 44 per cent was still unlet at that time. The largest construction activities are taking place in the regions of Berlin (around 152,000 m²) and Düsseldorf (around 116,000 m²). "In view of lower construction costs and the improved financing environment, developers are now being asked to realise new projects again," says Schekahn. "As soon as the economic situation makes it possible for users or the pressure grows to realise their previously paused property decisions, demand is likely to exceed supply. The projects in demand must now be initiated."

While year-on-year increases in prime rents for space of more than 5,000 m² of between 2.9 per cent and four per cent were observed in four of the five major regions, there was only one increase in Berlin in the last three months, at 24 per cent to EUR 10.50/m². This means that the gap between Berlin and Munich, where the highest rents in Germany are realised at EUR 10.70/m², has narrowed considerably. Düsseldorf follows with 9.00 euros/m², Hamburg with 8.50 euros/m² and Frankfurt with 7.95 euros/m².

Take-up is also below average outside the Big 5

Around 3.15 million m² was taken up outside the five major conurbations in the first three quarters, of which around 945,000 m² was accounted for by owner-occupiers (30 per cent of take-up). Overall, the previous year's figure of 3.68 million m² was missed by 14 per cent and the five-year average by 22 per cent.

More than one million square metres each were taken up by companies from the transport, traffic and warehousing sectors (35 percent of take-up) and industry (33 percent). Although retail companies were responsible for some large deals, their share was slightly lower at 24 per cent. The two largest deals were concluded by car manufacturers: BMW is building around 150,000 m² in Straßkirchen and Mercedes-Benz is renting around 124,000 m² in a project development in Bischweier in order to consolidate several warehouse locations. The next largest deals came from retail companies, including Galaxus in Neuenburg am Rhein (90,000 m²) and Fressnapf in Nörvenich (approx. 69,000 m²) in the first quarter and Nordwest Handel (approx. 68,000 m²) and Lidl in Hückelhoven (approx. 64,000 m²) in the second quarter.

At 295,300 m², the Ruhr area recorded the highest take-up result among the regions outside the five conurbations, but was down 20 per cent year-on-year. The Cologne and Leipzig/Halle regions followed with 216,600 m² and 170,200 m² respectively. Around two thirds of take-up of 5,000 m² or more was in new builds or project developments - in the size category of 50,000 m² or more, all transactions were in this category.

Contact: Sarina Schekahn, Head of Industrial & Logistics Agency JLL Germany

Phone: +49 (0) 40 350011 149

Email: sarina.schekahn@jll.com

About JLL

For more than 200 years, JLL (NYSE: JLL), a leading global commercial property and investment management firm, has helped clients acquire, build, occupy, manage and invest in a wide range of commercial, industrial, hospitality, residential and retail properties. As a Fortune 500® company with annual revenues of $20.8 billion and offices in more than 80 countries worldwide, our approximately 110,000 employees offer the power of a global platform combined with local expertise. Driven by our mission to shape the future of property for a better world, we help our clients, employees and society - true to our motto "SEE A BRIGHTER WAY". JLL is the brand name and a registered trademark of Jones Lang LaSalle Incorporated.

All contact details and press information for JLL Germany can be found at: jll.de/press.

Latest Warehouse News

Topping-out ceremony for Panattoni Park Lübeck Süd: New location with international prospects

The modern logistics and production site with a total area of around 46,000 m² is located in the newly developed Semiramis industrial park, one of the last large industrial areas in the Hanseatic city...

The Evolution of Commerce, the "Slow Rise" of AI, and Hyper-Personalization: Supply Chain and Retail Predictions for 2026

Technological advancements remain rapid, global dynamics are changing almost daily, and consumer expectations are changing faster than at any time in retail history...

Successful completion: Panattoni sells innovative multi-tenant project in Berlin to DWS

The fully let Panattoni Campus Berlin Zentrum has been successfully sold to DWS Group, a leading asset manager in Europe with a global reach....

Panattoni realises modern bakery for Edeka Südwest

Edeka Südwest will rely on a new, state-of-the-art production site for this purpose in the future...