European logistics market remains stable with take-up of 27 million m² and investment volume of € 56 billion despite economic slowdown

Paris, 3 March 2023 - The European logistics market proved to be resilient despite the difficult political and economic environment. Low vacancy rates and a shortage of land continue to drive up rents. This trend is being reinforced by rising construction costs. The prospects of further rent increases are encouraging investors, which is why the capital markets across Europe recorded high transaction volumes - despite a slowdown at the end of 2022 as part of the price correction. This is the result of an analysis by BNP Paribas Real Estate.

in 2022, the logistics market in the six leading European markets (Germany, France, the UK, the Netherlands, Poland and Spain) recorded a decline of 10%, but was still above the 5-year average. The total volume of 27 million m² (space from 5,000 m²) is impressive in addition to the exceptional result of 2021. "Economic growth in 2022 continued to support the letting markets, although take-up declined in some countries. Tenant demand for space to increase efficiency increased. Structural changes in consumer behaviour favoured the further growth of online retail, which further increased the demand for logistics space. Construction times and the availability of land are decisive factors in markets where the vacancy rate is well below the European average of 4%. New project developments are still lagging behind demand and few speculative projects are being launched," says Craig Maguire, Head of European Logistics at BNP Paribas Real Estate.

In Germany, the logistics market developed particularly dynamically in 2022 and fell just short of the 8 million sqm mark. However, it clearly exceeded the average result of 6 million m² from 2017 to 2020. The slowdown in momentum in the second half of the year is primarily due to the lack of supply, which is becoming increasingly noticeable in the relevant markets. The rise in construction costs led to significant rent increases in Hamburg, Munich and Cologne.

The letting market in the UK recorded a decline of 19% in 2022, but was able to maintain its momentum following the exceptional take-up of space in the previous year. The take-up of 4.9 million m² is due in particular to structural growth in the online retail sector and the optimisation of supply chains. The acute shortage of new build space is driving the strong rental growth.

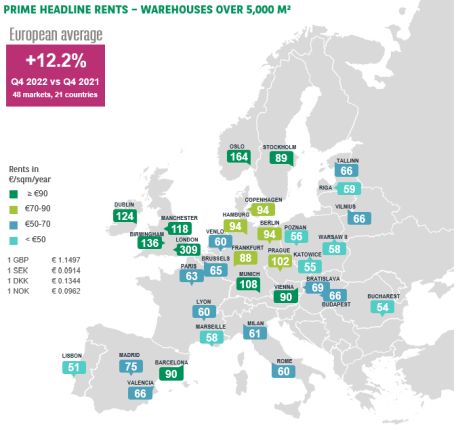

In Poland, take-up fell by 21%, but reached 4.5 million m², the second-highest result in its history. The market remained dynamic, but lost some momentum in the second half of the year. Rents are under pressure due to low vacancy rates and rising costs. As a result, prime rents rose sharply in 2022 in the most important logistics locations (from €41-44/m²/year to €49-59/m²/year). In Warsaw, the prime rent rose to €117/m²/year.

In France, take-up fell by only 13% to 3.9 million m². The strong demand for large warehouses gave the market an additional boost at the beginning of the year, but stabilised in the second half of the year. Supply remains tight in most markets, meaning that the vacancy rate is at an all-time low of less than 3%. Due to the ongoing intense competition for first-class properties, rents are expected to rise in prime locations.

In the Netherlands, take-up rose by 3% to 3.6 million m². The supply of newly built warehouses is becoming increasingly scarce, meaning that tenants are increasingly opting for high-quality existing properties. Robust demand and the shortage of supply continue to put pressure on rents.

In Spain, take-up increased by 8% to 2.3 million m². The market set another record in 2022 and recorded one of the strongest performances in Europe. Market activity was boosted in particular by e-commerce and food retail. The low vacancy rates mean there is potential for further rent increases.

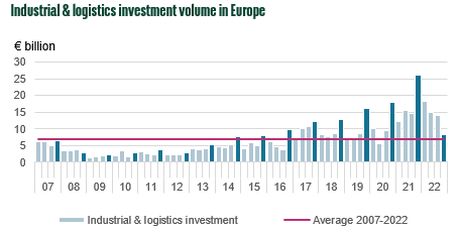

The investment volume in the industrial and logistics segment reached its second-highest level in history, even though market momentum is slowing significantly

In 2022, the investment volume fell by 19% to €56 billion, although it was almost €15 billion higher than the annual average for 2017 to 2020. "Even after five years in which outstanding investment volumes were achieved, the market remains attractive to buyers. However, the investment market has been challenged by the increasing shortage of supply and fundamental changes in the macroeconomic and financial environment," says Craig Maguire. The return to monetary normality at a global level has seen interest rates rise to pre-global financial crisis levels in less than six months. The risk premium has fallen significantly due to the sharp rise in interest rates on 10-year bonds. The rapid rise in interest rates led to a price correction, which affected the logistics segment the most of all property sectors. The investment freeze led to a significant increase in logistics yields.

This trend could continue, at least until the end of the interest rate hikes, which most forecasts predict will take place by mid-2023. A large part of the increase in yields for prime properties is likely to have already taken place, while prices for properties outside the prime segment will probably still be negotiated intensively in 2023.

The investment market for industry and logistics in the UK recorded a sharp decline in investment volume compared to the previous year (-32% to €14.4 billion in 2022). This is due to unsuccessful negotiations and properties being withdrawn from the market. The prime yield increased by 175 basis points in 2022. Germany achieved a record volume of € 10.1 billion. This result is primarily due to major deals in the first quarter. The prime yield has risen by 85 basis points and a further increase can also be expected this year. In France, there was only a slight decline of 6% to € 6.4 billion due to the strong market dynamics. Prime yields rose by 60 basis points to 3.80% in 2022. This trend is likely to continue in 2023.

Market activity in the Netherlands was mostly good until it also slowed down in the fourth quarter. In view of the strong demand, the yield adjustment in the first half of 2023 could lead to a boost in investment activity.

Italy also saw record volumes last year, with the 28% increase attributable to portfolio deals. The yield rose by 40 basis points to 4.4%.

In Spain, the investment volume fell by 40% in 2022, but was still above the 5-year average. The decline in the final quarter led to an increase in the prime yield for big box properties of 95 basis points.

After the record result from 2021, Poland achieved a 16% lower result, which at €1.8bn is roughly in line with the annual average since 2017.

PS: The graphics may be used in the context of reporting on this topic, provided the source BNP Paribas Real Estate is cited.

European logistics market remains stable with take-up of 27 million m² and investment volume of € 56 billion despite economic slowdown | BNP Paribas Real Estate

Press contact:

Chantal Schaum - Tel: +49 (0)69-298 99-948, Mobile: +49 (0)174-903 85 77, chantal.schaum@bnpparibas.com

Viktoria Gomolka - Tel: +49 (0)69-298 99-946, Mobile: +49 (0)173-968 60 86, viktoria.gomolka@bnpparibas.com

Melanie Engel - Tel: +49 (0)40-348 48-443, Mobile: +49 (0)151-117 615 50, melanie.engel@bnpparibas.com

About BNP Paribas Real Estate

BNP Paribas Real Estate is a leading international property services provider that offers its clients comprehensive services in all phases of the property cycle: Transaction, Consulting, Valuation, Property Management, Investment Management and Property Development. With 5,000 employees, the company supports owners, tenants, investors and the public sector in their projects thanks to local expertise in 30 countries (own locations and alliance partners) in Europe, the Middle East and Asia. BNP Paribas Real Estate is part of the BNP Paribas Group, a leading global financial services provider.

As part of its commitment to sustainable cities, BNP Paribas Real Estate aims to play a leading role in the transition to creating more sustainable real estate that is low-carbon, resilient, inclusive and conducive to well-being. To this end, the company has developed a CSR policy with the following four objectives: to improve the economic performance and use of buildings in an ethical and responsible manner; to enable a low-carbon transition and reduce the environmental footprint; to ensure the development, engagement and well-being of employees; and to be an active player in the property sector, building and promoting local initiatives and partnerships.

Further information: www.realestate.bnpparibas.com/

About BNP Paribas in Germany

BNP Paribas is a leading European bank with an international reach. The BNP Paribas Group has been active in Germany since 1947 and has successfully positioned itself in the market with 12 business units. Private, corporate and institutional clients are served by around 6,000 employees nationwide in all relevant economic regions. www.bnpparibas.de

Latest Warehouse News

Topping-out ceremony for Panattoni Park Lübeck Süd: New location with international prospects

The modern logistics and production site with a total area of around 46,000 m² is located in the newly developed Semiramis industrial park, one of the last large industrial areas in the Hanseatic city...

The Evolution of Commerce, the "Slow Rise" of AI, and Hyper-Personalization: Supply Chain and Retail Predictions for 2026

Technological advancements remain rapid, global dynamics are changing almost daily, and consumer expectations are changing faster than at any time in retail history...

Successful completion: Panattoni sells innovative multi-tenant project in Berlin to DWS

The fully let Panattoni Campus Berlin Zentrum has been successfully sold to DWS Group, a leading asset manager in Europe with a global reach....

Panattoni realises modern bakery for Edeka Südwest

Edeka Südwest will rely on a new, state-of-the-art production site for this purpose in the future...