Logistics space turnover recovers in the third quarter

Annual forecast raised to a good six million m²

FRANKFURT, 3 November 2023 - Around 4.73 million m² (owner-occupiers and lettings) were taken up on the German market for warehouse and logistics space in the first three quarters of 2023. The third quarter accounts for a significant proportion of this: at 2.04 million m², take-up was significantly higher than the first two quarters of the year, at 1.43 and 1.26 million m² respectively. This was the first time in four quarters that the two million square metre mark was exceeded.

Nevertheless, the first nine months of last year were significantly better, with this year's period falling short of the result by 30 per cent. The declines are more moderate compared to the five-year average of 17 per cent and the ten-year average of eight per cent. The number of contracts concluded also fell moderately: 530 contracts correspond to a decline of around twelve per cent.

"The stronger third quarter is evidence of sustained demand on the market for warehouse and logistics space. High pre-letting rates and rising rents show that suitable space is in short supply and users are willing to pay correspondingly high rents for a suitable property," says Sarina Schekahn, Head of Industrial & Logistics Agency JLL Germany. "Due to the weaker first half of the year, we will not be able to match the annual take-up of previous years, but we are confidently forecasting a good six million sqm for 2023 as a whole."

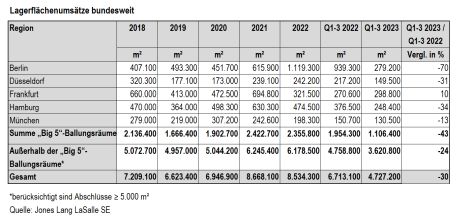

In the five property strongholds (Berlin, Düsseldorf, Frankfurt, Hamburg and Munich), around 1.11 million m² was taken up in the first three quarters, 43 per cent less than in the first nine months of the previous year and around a third less than the five-year average. The region with the highest take-up was Frankfurt with 298,800 m² and a year-on-year increase of ten per cent. All other regions recorded a double-digit percentage drop in the same period: 130,500 m² (minus 13 per cent) was taken up in Munich, 149,500 m² in Düsseldorf (minus 31 per cent) and 248,400 m² (minus 34 per cent) in Hamburg. In Berlin, the drop was as high as 70 per cent to 279,200 m²: the record result in the previous year due to the owner-occupier Tesla in Grünheide, which alone accounted for around 327,000 m², had a significant impact.

No deals of more than 40,000 m² were registered in the Big 5 in the first nine months of 2023, compared to four contracts totalling 462,000 m² in the same period of the previous year. The largest deal in the current year was signed by a logistics service provider, which took around 38,000 m² at Magna Park in Werder near Berlin. The next two largest lettings are also accounted for by logistics companies with around 34,000 m² in Dormagen near Düsseldorf and around 33,000 m² also in Werder near Berlin. Accordingly, companies from the transport, traffic and warehousing sector lead the sector statistics with a share of 38 per cent. Industrial and retail companies follow with 26 and 19 per cent respectively.

Prime rents continue to rise

There were also significant declines in completions: At around 472,000 m², only around half as much warehouse space was completed in the five property strongholds between January and September 2023 as in the same period last year. Only 20 per cent of this space was available at the time of completion. Of the 700,000 m² currently under construction, around 41 per cent is currently unlet.

Year-on-year, prime rents for warehouse space of 5,000 m² or more have risen in all five metropolises. The strongest increases were seen in Düsseldorf at 29.6 per cent (EUR 8.75/m²) and Munich at 25.9 per cent (EUR 10.70/m²). In Berlin, the figure rose by 15.4 per cent (EUR 7.50/m²), in Hamburg by ten per cent (EUR 8.25/m²) and in Frankfurt by 4.1 per cent (EUR 7.60/m²).

"There is currently no sign of an end to rising prime rents. The decline in completions and the small amount of space under construction - particularly of a speculative nature - are likely to exacerbate the situation. The high prime rents in Munich in particular, which continue to rise sharply, illustrate the ongoing pressure on users and the challenge of finding or creating modern and ESG-compliant space in southern Germany," says Schekahn. "The situation is different in western and eastern Germany: project developments continue to take place in the east in particular, and we are also seeing an increase in subletting here."

Ruhr no longer the strongest region

Outside the five property strongholds, a volume of around 3.62 million m² of space was taken up in the first nine months of 2023. However, even there the previous year's figure was missed by 24 per cent and the five-year average by around eleven per cent. The third quarter also accounted for a significant share of take-up at 45 per cent. The two largest deals in the first nine months were also concluded during this period: Daimler Truck began construction of a logistics centre of around 260,000 m² in Halberstadt near Magdeburg, while VW is building a 210,000 m² facility in Salzgitter.

The dynamic performance of the automotive industry from the first half of the year is thus continuing, with four of the five largest deals in the first nine months being concluded by well-known representatives from this sector. Industrial companies accounted for around 41 per cent of take-up outside the conurbations under review, significantly more than the five-year average (28 per cent). "The automotive segment is currently particularly space-intensive due to the parallel production of combustion and electric cars. However, locations with sufficient space are hardly available in the five property strongholds, and manufacturers are instead moving to regions that can score points with better availability and good connections at significantly lower prices," says Schekahn. "As a result, manufacturers are creating new logistics network structures, which will then lead to more efficient and easier leasing of locations in these regions in the future."

Automotive is followed by users from the transport, traffic and warehousing sector with a share of 29 per cent and retail companies with 25 per cent. The largest deals in these sectors include the letting of around 74,000 m² by logistics service provider Rhenus in Sülzetal near Magdeburg and the establishment of an online retailer in Horn-Bad Meinberg, which is building a logistics centre of around 175,000 m² there.

Hannover/Braunschweig tops the list of regions for the first time with around 447,000 m². It thus relegates the Ruhr region (around 395,000 m²) to second place, which has led the statistics since 2016. The aforementioned completion by VW in Salzgitter and the start of construction of a 40,000 m² logistics centre by Aldi Nord in Lehrte are among the largest take-ups in Hannover/Braunschweig. The Osnabrück/Münster (279,000 m²) and Leipzig/Halle (225,000 m²) regions follow some way behind. 69 per cent of take-up was in new builds or project developments, and 100 per cent for space of more than 50,000 m².

About Jones Lang LaSalle

For more than 200 years, JLL (NYSE: JLL), a leading global commercial property and investment management firm, has helped clients acquire, build, occupy, manage and invest in a wide range of commercial, industrial, hotel, residential and retail properties. As a Fortune 500® company with annual revenues of $20.9 billion and offices in more than 80 countries worldwide, our approximately 105,000 employees offer the power of a global platform combined with local expertise. Driven by our goal of shaping the future of property for a better world, we help our customers, employees and society - true to our motto "SEE A BRIGHTER WAY".

Contact:

Sarina Schekahn, Head of Industrial & Logistics Agency JLL Germany

Phone: +49 (0) 40 350011 149

Email: sarina.schekahn@jll.com

Latest Warehouse News

Topping-out ceremony for Panattoni Park Lübeck Süd: New location with international prospects

The modern logistics and production site with a total area of around 46,000 m² is located in the newly developed Semiramis industrial park, one of the last large industrial areas in the Hanseatic city...

The Evolution of Commerce, the "Slow Rise" of AI, and Hyper-Personalization: Supply Chain and Retail Predictions for 2026

Technological advancements remain rapid, global dynamics are changing almost daily, and consumer expectations are changing faster than at any time in retail history...

Successful completion: Panattoni sells innovative multi-tenant project in Berlin to DWS

The fully let Panattoni Campus Berlin Zentrum has been successfully sold to DWS Group, a leading asset manager in Europe with a global reach....

Panattoni realises modern bakery for Edeka Südwest

Edeka Südwest will rely on a new, state-of-the-art production site for this purpose in the future...