Logistics investment market adjusts to new activity - fewer deals at the end of the first half of the year - more pitches and marketing launches registered

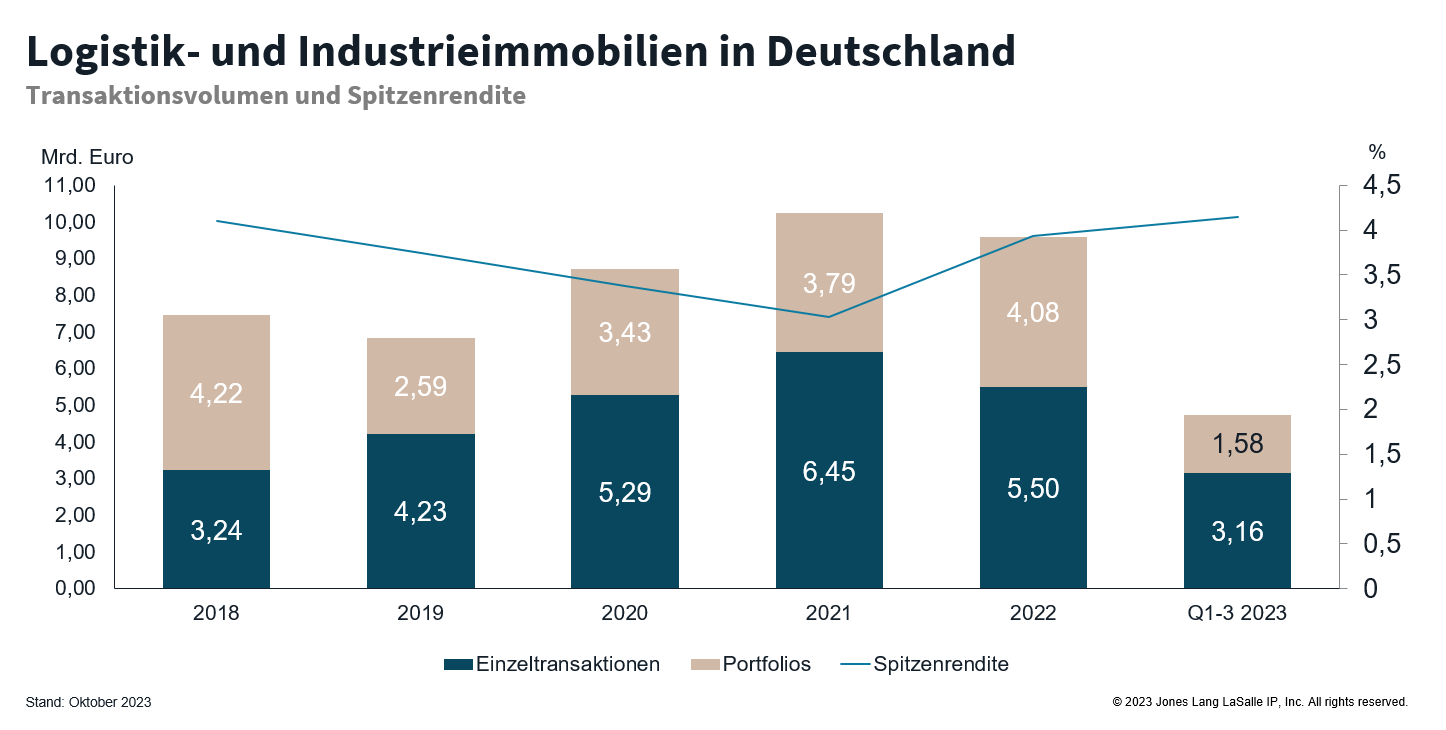

FRANKFURT, 14 July 2023 - The German investment market for logistics and industrial properties grew only very slightly in the second quarter of 2023: With a transaction volume of around 1.1 billion euros, the starting quarter was exceeded by around 90 million euros. This brings the total volume for the first half of the year to around 2.2 billion euros - a year-on-year decline of 62 per cent. However, 2022 was a particularly strong investment year, which is why the losses are more moderate compared to the five-year average of minus 43 per cent and the ten-year average of minus 30 per cent. The first half of 2016 was weaker, with a transaction volume of €1.85 billion.

Diana Schumann, Co-Head of Industrial & Logistics Investment JLL Germany: "Although the difference in transaction volumes in the first two quarters is small, it underlines the sustained demand and an intact market in which sellers and buyers can agree on pricing. We are currently observing that the activity of market participants has clearly picked up again. The number of pitches has risen significantly compared to previous quarters, as has the number of individual properties currently being marketed and the first larger portfolios. We are therefore raising our forecast for the year to six billion euros."

70 transactions were recorded in the second quarter of 2023, significantly more than in the first quarter with 53. 123 deals were recorded in the first half of the year, compared to 29 more in the same period of the previous year. However, the number of large transactions is more significant: While two deals worth more than €100 million were counted in the first quarter of 2023 - including the Areal Böhler in Düsseldorf and the Bauknecht Business Park in Stuttgart's Fellbach submarket - this size category was not reached in the second quarter. In the same period of the previous year, there were eleven major transactions. As a result, the share of the five largest deals in the total volume shrank from 34 per cent in the first half of the previous year to 23 per cent in the current year.

Dominic Thoma, Co-Head of Industrial & Logistics Investment JLL Germany: "The slightly higher transaction volume in the second quarter was achieved entirely without major transactions. Investors are only returning to the market from the sidelines with a certain degree of caution, especially when it comes to large individual properties, and are currently only willing to venture into the market with higher yields. The preference is clearly for smaller volumes of 20 to 60 million euros. The situation is different for portfolios. Here, the number of pitches has increased and several portfolios are already being marketed or are about to be signed, so we will see more large transactions in the coming quarters."

Investors are looking for higher returns, but are still taking little risk

At 58 per cent, the majority of investors in the first half of the year came from Germany; on the seller side, their share was slightly higher at 64 per cent. On balance, foreign investors increased their holdings of logistics and industrial properties by 140 million euros. Investors focussed in particular on top products in the first half of the year: Core investments were the most popular at 41 per cent, while core-plus properties were in similarly high demand with a share of 39 per cent. The share of value-add properties was significantly lower at twelve per cent.

Diana Schumann explains: "The ongoing caution on the market is also having an impact on the risk classes. Investors continue to target high-quality core properties in good locations in order to secure them at the currently attractive conditions. However, sellers are still holding back these properties unless they are in urgent need of liquidity. This means that top properties are usually only placed on the market by developers. However, these new buildings are already ESG-compliant, which has almost become a necessity for core products over and above the standard criteria."

However, there is an even greater focus on core-plus and value-add properties in order to achieve even higher returns, particularly through rent adjustments, extensions or manage-to-green, says Thoma. "There is a lot of potential for value appreciation, particularly due to the shortage of space, good demand in or near city centres and rental growth in recent years. "

While the prime yields for top products in the seven property strongholds were still at 3.90 and 3.95 per cent in the previous quarter, they rose by ten basis points to 4.00 and 4.05 per cent respectively in the past quarter due to the slight increase in financing costs. The prime yields for logistics and industrial properties last stood at 4.00 per cent in the first quarter of 2019, up 90 and 95 basis points respectively compared to the same quarter of the previous year.

"The market is currently being given a new direction in terms of pricing and yield expectations," says Thoma. "The rapid rise in interest rates began more than a year ago, followed by high volatility. However, the steady rises and falls are levelling out more and more. At just over three per cent, the 5-year swap is currently as high as it was around twelve years ago, but it is now more of a sideways movement and therefore a signal of stability. If, as expected, the ECB's next interest rate hikes are only minor and the banks' margins for logistics continue to fall, the bottom of the price declines could already have been reached. Otherwise, the prime yield will only rise slightly by the increase in financing costs."

"Logistics and industrial properties are still at the top of investors' acquisition lists precisely because of the rapid price adjustment and the favourable framework data. Although the transaction volume to date does not yet reflect this, it is also an indication of supply for attractive properties in good locations, and competition among bidders is increasing again," says Schumann. There are also an increasing number of investors entering the segment for the first time. "Conservative, equity-rich core investors in particular are looking for alternatives in logistics and industry to asset classes that are currently weakening. This further differentiates the investor base and yield expectations and helps to find the right investor for each property."

Contact: Dominic Thoma, Co-Head of Industrial & Logistics Investment JLL Germany

Phone: +49 (0) 89 290088 127

Email: dominic.thoma@jll.com

Contact: Diana Schumann, Co-Head of Industrial & Logistics Investment JLL Germany

Phone: +49 (0) 211 13006 410

Email: diana.schumann@jll.com

Latest Warehouse News

Topping-out ceremony for Panattoni Park Lübeck Süd: New location with international prospects

The modern logistics and production site with a total area of around 46,000 m² is located in the newly developed Semiramis industrial park, one of the last large industrial areas in the Hanseatic city...

The Evolution of Commerce, the "Slow Rise" of AI, and Hyper-Personalization: Supply Chain and Retail Predictions for 2026

Technological advancements remain rapid, global dynamics are changing almost daily, and consumer expectations are changing faster than at any time in retail history...

Successful completion: Panattoni sells innovative multi-tenant project in Berlin to DWS

The fully let Panattoni Campus Berlin Zentrum has been successfully sold to DWS Group, a leading asset manager in Europe with a global reach....

Panattoni realises modern bakery for Edeka Südwest

Edeka Südwest will rely on a new, state-of-the-art production site for this purpose in the future...