BNP Paribas Real Estate publishes logistics market data for the first three quarters of 2025

Take-up increases significantly year-on-year

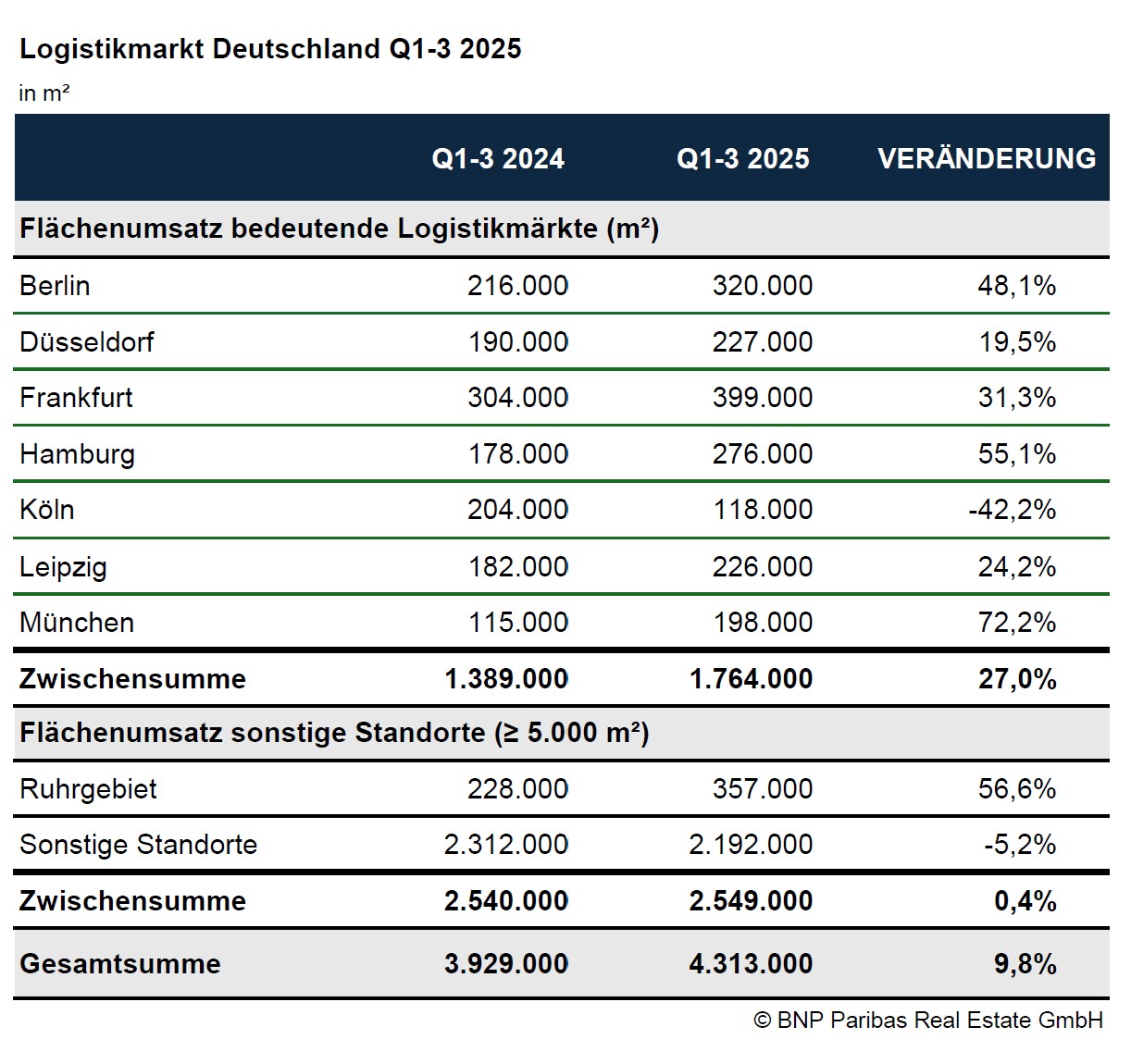

By the end of the 3rd quarter, the nationwide logistics market had achieved take-up of 4.3 million m², exceeding the previous year's result by around 10%. After a somewhat subdued start to the year, the market picked up in the course of the year and increased take-up in the following quarters to 1.5 million m² in the second quarter and 1.6 million m² in the third quarter. Against the backdrop of the still weak economic environment, this result can be seen as very positive – even if it still deviates by 14% from the ten-year average. This is the result of the analysis by BNP Paribas Real Estate.

"Since the second quarter, there has been more activity and a better mood on the part of companies on the market than in the weak previous year. This is reflected, among other things, in a higher number of large-scale contracts and an increasing number of applications for space. It is noteworthy that there is also more demand for space from the e-commerce sector," explains Christopher Raabe, Managing Director and Head of Logistics & Industrial at BNP Paribas Real Estate GmbH.

It is mainly the top logistics markets (Berlin, Düsseldorf, Frankfurt, Hamburg, Cologne, Leipzig and Munich) that have increased significantly year-on-year with an increase of 27% and, with a total of just under 1.8 million m², are only 4% below their long-term average. Frankfurt clearly leads the ranking with take-up of 399,000 m² (+31% compared to the same period last year) and relegates Berlin (320,000 m²; +48%) and Hamburg (276,000 m²; +55%) to second and third place despite significant increases in take-up. At 227,000 m² or +19%, Düsseldorf also recorded a significant increase compared to the same period last year and was the only major logistics hub to achieve a result of 24% that was noticeably above the ten-year average. Leipzig grew by 24% to 226,000 m², and Munich also benefited from larger deals in the third quarter, resulting in a significant increase of +72% and an average take-up of 198,000 m². Cologne has not yet been able to build on the high result of the previous year and is the only top location to record a minus compared to the previous year (118,000 m², -42%). Thanks to a number of larger deals, the Ruhr region is around 57% above the same period last year with take-up of 357,000 m² and is already at the level of annual take-up in 2024 at the end of September.

The most important demand group in the current period under review is logistics service providers. With a share of 41% of take-up, they are well ahead of the other sectors and achieve an above-average take-up result in absolute figures. Numerous large-scale contracts – including from companies in Asia – have contributed to this development. Since they also handle the business of trading companies, among other things, this puts the still comparatively small share of this industry of just under 21% into perspective. The production companies, which were very strong in the two previous years, are now close to their long-term average with a current share of 30%.

Rents rose slightly again in some markets in the third quarter. Compared with the previous year, the increase in prime rents was 2.4% on average across all locations. At €10.70/m² (+2%), Munich continues to be by far the most expensive market. Frankfurt rises to €8.50/m², reaching the level of Düsseldorf and Hamburg. While 8.20 €/m² is achieved at its peak in Berlin, the top rent in the Ruhr area has climbed to 8 €/m². In Cologne, the prime rent rises by 3% to €7.90/m², and in Leipzig, €5.70/m² remains unchanged. Average rents have also risen, with an increase of 3.9% year-on-year and on average across all major locations.

Prospects

The nationwide logistics market is currently in solid shape, defying the still challenging conditions. In addition to the lack of economic tailwind as well as the various geopolitical crises and armed conflicts, US customs policy also remains a factor of uncertainty for companies.

On the other hand, the German special funds for infrastructure and climate neutrality as well as the financial leeway for defence spending have had a positive effect on business sentiment, but the delay in concrete investments is expected to provide stimulating impulses, especially from 2026 onwards. In addition, positive effects are expected from the implementation of necessary reforms to strengthen the business location, so that higher economic growth is expected from next year onwards and, in the course of this, higher take-up of space again. Increased demand is already being recorded from the armaments and defence segment in particular – a trend that is expected to intensify from next year.

"For the current year, it can be assumed that demand will continue to develop robustly until the end of the year and that take-up is likely to remain stable at least at the level of the past two quarters. However, the final quarter can often increase significantly again, so that there is a realistic chance that total take-up will approach a volume of 6 million m² somewhat more strongly again. A broad increase in sales outside the major logistics strongholds would be an important prerequisite for this. However, the weak previous year's result of 5.3 million m² was to be significantly exceeded. In terms of rental prices, further slight upward adjustments are possible, especially in markets with a limited modern supply of space," says Bastian Hafner, Head of Logistics & Industrial Advisory at BNP Paribas Real Estate GmbH, summarising the further outlook.

You can also find all market reports on our homepage www.realestate.bnpparibas.de

About BNP Paribas Real Estate

BNP Paribas Real Estate is a leading international real estate services provider that offers its clients comprehensive services at all stages of the real estate cycle: Transaction, Consulting, Valuation, Property Management, Investment Management and Property Development. With 4,000 employees, the company supports owners, tenants, investors and the public sector in their projects thanks to local expertise in 23 countries (own locations and alliance partners) in Europe, the Middle East and Asia. BNP Paribas Real Estate is part of the BNP Paribas Group, a leading global financial services provider.

As part of its commitment to sustainable cities, BNP Paribas Real Estate aims to take a leading role in the transition to creating more sustainable properties that are low-carbon, resilient, inclusive and conducive to well-being. To this end, the company has developed a CSR policy with the following four objectives: to improve the economic performance and use of buildings in an ethical and responsible way, to enable a low-carbon transition and reduce the environmental footprint, to ensure the development, engagement and well-being of employees, as well as to be an active player in the real estate sector, and to establish and promote local initiatives and partnerships.

About BNP Paribas in Germany

BNP Paribas is a leading provider of banking and financial services in Europe. The company operates in 64 countries and employs almost 178,000 people, including more than 144,000 in Europe. The BNP Paribas Group has been active in Germany since 1947 and has successfully established itself on the market with a wide range of services from networked business units. Private customers, companies and institutional customers are served by around 6,000 employees nationwide in all relevant economic regions. BNP Paribas' broad range of products and services is equivalent to that of an innovative universal bank.

Further information: www.bnpparibas.de

Further information: www.realestate.bnpparibas.com

Press:

Chantal Schaum – Tel: +49 (0)69-298 99-948, Mobile: +49 (0)174-903 85 77, chantal.schaum@bnpparibas.com

Pia Ewald – Tel: +49 (0)69-298 99-941, Mobile +49 (0)160-905-800-19, pia.ewald@bnpparibas.com

Latest Warehouse News

Topping-out ceremony for Panattoni Park Lübeck Süd: New location with international prospects

The modern logistics and production site with a total area of around 46,000 m² is located in the newly developed Semiramis industrial park, one of the last large industrial areas in the Hanseatic city...

The Evolution of Commerce, the "Slow Rise" of AI, and Hyper-Personalization: Supply Chain and Retail Predictions for 2026

Technological advancements remain rapid, global dynamics are changing almost daily, and consumer expectations are changing faster than at any time in retail history...

Successful completion: Panattoni sells innovative multi-tenant project in Berlin to DWS

The fully let Panattoni Campus Berlin Zentrum has been successfully sold to DWS Group, a leading asset manager in Europe with a global reach....

Panattoni realises modern bakery for Edeka Südwest

Edeka Südwest will rely on a new, state-of-the-art production site for this purpose in the future...