Logistics investment market starts to recover - also thanks to major transactions

Four of the five largest deals in the first nine months of 2023 took place in the third quarter

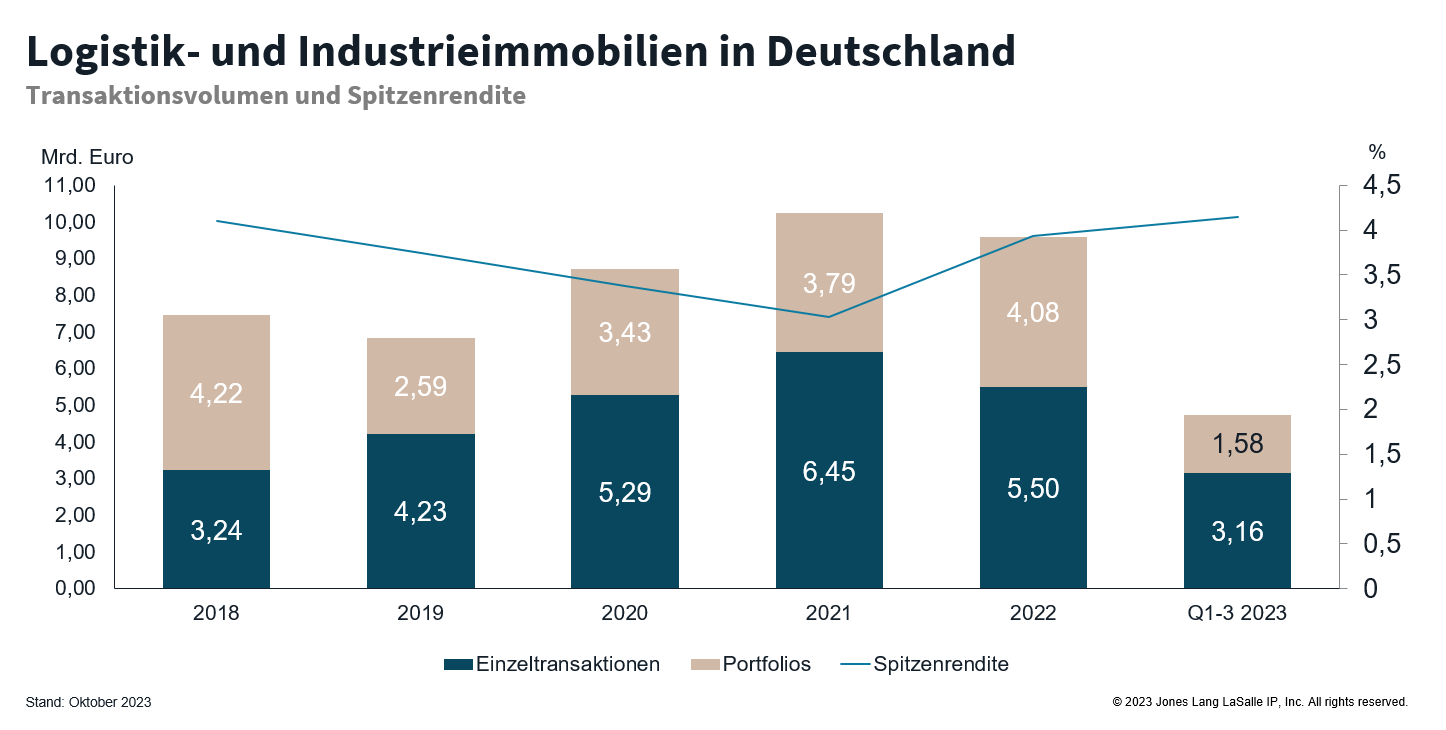

FRANKFURT, 8 November 2023 - The German investment market for logistics and industrial properties saw a significantly higher transaction volume in the third quarter of 2023. At 2.6 billion euros, it significantly surpassed the first two quarters of the year with around one billion euros each. This means that the logistics investment market recorded a transaction volume of around 4.7 billion euros in the first nine months and, for the first time after three quarters, is the second strongest asset class after Living with 6.6 billion euros.

Although the first nine months of 2023 are around 38 per cent behind the same period of the previous year, this is largely due to the weak first half of the year. The five-year average was also underperformed by 20 per cent. Compared to the past ten years, however, there was an increase of three per cent

Dominic Thoma, Co-Head of Industrial & Logistics Investment JLL Germany: "The significantly higher transaction volume in the third quarter is the result of the resumption of market activity since the beginning of the year. It takes around four to six months from the marketing go-ahead to completion. In the second half of 2022, many market participants were still on the sidelines, which meant that significantly fewer sales were brought to the market. This resulted in the weak transaction volume in the first half of 2023. The market has been much more buoyant again since the beginning of the year and numerous deals have now been brought to the notary."

"Due to both rising and fluctuating interest rates, investors and buyers found it difficult to join hands last year. Offers and calculations only had a short half-life and the parties often did not come together, which meant that deals collapsed," says Thoma. "The interest rate swing is now almost over. Although the only slight increase still has an influence on the price level, it has made it possible for everyone involved to plan more accurately."

Diana Schumann, Co-Head of Industrial & Logistics Investment JLL Germany: "We are forecasting a transaction volume of 6.5 billion euros for 2023 as a whole. However, given the return of activity, there is also potential for seven billion euros. The final figure will not depend on demand, but on which transactions are completed this year and which slip into 2024."

Joint ventures and portfolio deals determine five largest deals

While 211 logistics and industrial property transactions were recorded in the first three quarters of the previous year, 186 were recorded in the same period this year. 64 of these deals were completed in the third quarter, 69 in the second quarter and 53 in the first. Accordingly, the average volume of individual transactions was higher in the third quarter than in the two previous quarters. However, the number of transactions in the three-digit million range is declining: while 15 deals of this size were registered between January and September 2022, there have been nine so far this year.

The return of market activity is also reflected in the fact that four of the five largest deals so far this year were concluded in the third quarter. Deka completed by far the largest transaction with the acquisition of shares in a portfolio from logistics developer VGP. Six project developments from DFI Real Estate were also transferred to the Hansa German Logistics Impact Fund, a joint venture between DFI and Hansainvest Real Assets. Clarion Partners Europe acquired a portfolio of five logistics properties from Blackstone and P3 secured the AXA/Baytree portfolio. Three of the four large portfolios are joint ventures. As in the same period of the previous year, the top 5 deals accounted for around 31 per cent of the total transaction volume.

The pipeline of project developments is currently well filled and there are several products for sale on the market, explains Thoma. "In addition to portfolio rationalisation by large portfolio holders who want to create new liquidity, the topic of sale-and-leaseback is becoming increasingly important. The financing of many companies is coming to an end, and in view of the high interest rates and lack of liquidity, the pressure to capitalise tied-up capital is increasing significantly."

Demand for products in the logistics sector is high and spread across all risk classes. "There are still few core properties on the market. Investors do not want to part with their expensively acquired treasures, especially as there are fewer buyers who are prepared to pay adequate top prices for them. However, this is likely to change again in the long term," says Thoma. At 22 per cent, core properties accounted for a much smaller share of the transaction volume than core-plus properties at 64 per cent. "Investors are much more liquid in the core-plus segment. In addition, numerous new projects have been developed in B and C locations, while hardly any A locations are coming onto the market. Although capital is also available in the value-add segment, financing conditions are more difficult there. Instead, many investors are trying to realise the potential of their properties themselves and sell them as core-plus," explains Thoma. Value-add and opportunistic products accounted for a share of seven per cent. Investors and sellers from Germany each accounted for 57 per cent.

Prime yields for offices almost at logistics level

Prime yields rose once again in all seven property strongholds, reaching 4.15 per cent across the board in the third quarter of 2023. Compared to the previous quarter, they rose by ten to 15 basis points; in the same quarter of the previous year, they stood at 3.40 and 3.45 per cent respectively. "In the office asset class, the prime yield in the seven property strongholds averages 4.12 per cent - just three basis points lower than logistics. Although the ECB's key interest rate has not been raised recently, financing conditions are nevertheless becoming even more difficult and the granting of financing is becoming more restrictive. In combination with currently still attractive alternative investments, yields remain under pressure, which is why a further increase of 25 basis points to an expected 4.40 per cent is to be expected by the end of the year," says Schumann.

In contrast to other asset classes, the logistics segment has been spared any particular challenges in the recent past: Rent caps, regulatory measures or home offices do not play a role in logistics, which is why the asset class remains comparatively safe. "In eastern Germany in particular, the project pipeline is well filled, including speculative developments. In large parts of western Germany, demand is high, exceeding supply and causing rental prices to rise further. There is therefore much to be said in favour of a logistics investment," says Schumann.

Contact:

Diana Schumann, Co-Head of Industrial & Logistics Investment JLL Germany

Phone: +49 (0) 211 13006 410

Email: diana.schumann@jll.com

Contact:

Dominic Thoma, Co-Head of Industrial & Logistics Investment JLL Germany

Phone: +49 (0) 89 290088 127

Email: dominic.thoma@jll.com

Jones Lang LaSalle SE

For more than 200 years, JLL (NYSE: JLL), a leading global commercial property and investment management firm, has helped clients buy, build, occupy, manage and invest in a wide range of commercial, industrial, hotel, residential and retail properties. As a Fortune 500® company with annual revenues of $20.9 billion and offices in more than 80 countries worldwide, our approximately 105,000 employees offer the power of a global platform combined with local expertise. Driven by our goal of shaping the future of property for a better world, we help our customers, employees and society - true to our motto "SEE A BRIGHTER WAY".

Latest Warehouse News

Topping-out ceremony for Panattoni Park Lübeck Süd: New location with international prospects

The modern logistics and production site with a total area of around 46,000 m² is located in the newly developed Semiramis industrial park, one of the last large industrial areas in the Hanseatic city...

The Evolution of Commerce, the "Slow Rise" of AI, and Hyper-Personalization: Supply Chain and Retail Predictions for 2026

Technological advancements remain rapid, global dynamics are changing almost daily, and consumer expectations are changing faster than at any time in retail history...

Successful completion: Panattoni sells innovative multi-tenant project in Berlin to DWS

The fully let Panattoni Campus Berlin Zentrum has been successfully sold to DWS Group, a leading asset manager in Europe with a global reach....

Panattoni realises modern bakery for Edeka Südwest

Edeka Südwest will rely on a new, state-of-the-art production site for this purpose in the future...