The Great Consolidation: Why Contract Logistics Will Change Its Face in 2026

Table of Contents

- Status quo: Who with whom? The actors at a glance

- Term check: Merger, takeover or cooperation?

- Was 2025 an exceptional year? A look back from the perspective of 2026

- The driving factors: Why the hunger for mergers?

- Change of perspective: What do those involved get out of it?

- Market impact: What does that do to the competition?

- International comparison: Germany vs. the world

- Case study: pfenning Group & Logosys – strategy instead of coincidence

- Conclusion: Strategic questions for logistics decision-makers in 2026

The logistics world in spring 2026 resembles a gigantic Tetris game for advanced players, which is now entering the decisive phase of integration. While global supply chains are looking for stability after the shocks of previous years, a tectonic shift has been taking place behind the scenes. Names such as DSV, DB Schenker, pfenning-Gruppe or Kuehne+Nagel dominate the headlines – no longer only through operational excellence, but also through completed megadeals and strategic realignments.

But what drives this hunger for greatness? Is it pure market power or the strategic compulsion to technological sovereignty? In this long-read, we analyse the background to the M&A wave (Mergers & Acquisitions), shed light on the differences in cooperation models and assess the market situation in 2026.

Status quo: Who with whom? The actors at a glance

While 2024 and 2025 were still years of announcements, 2026 is the year of the operational merger. The list of players has been consolidated, but new names have also been added.

Current examples and milestones:

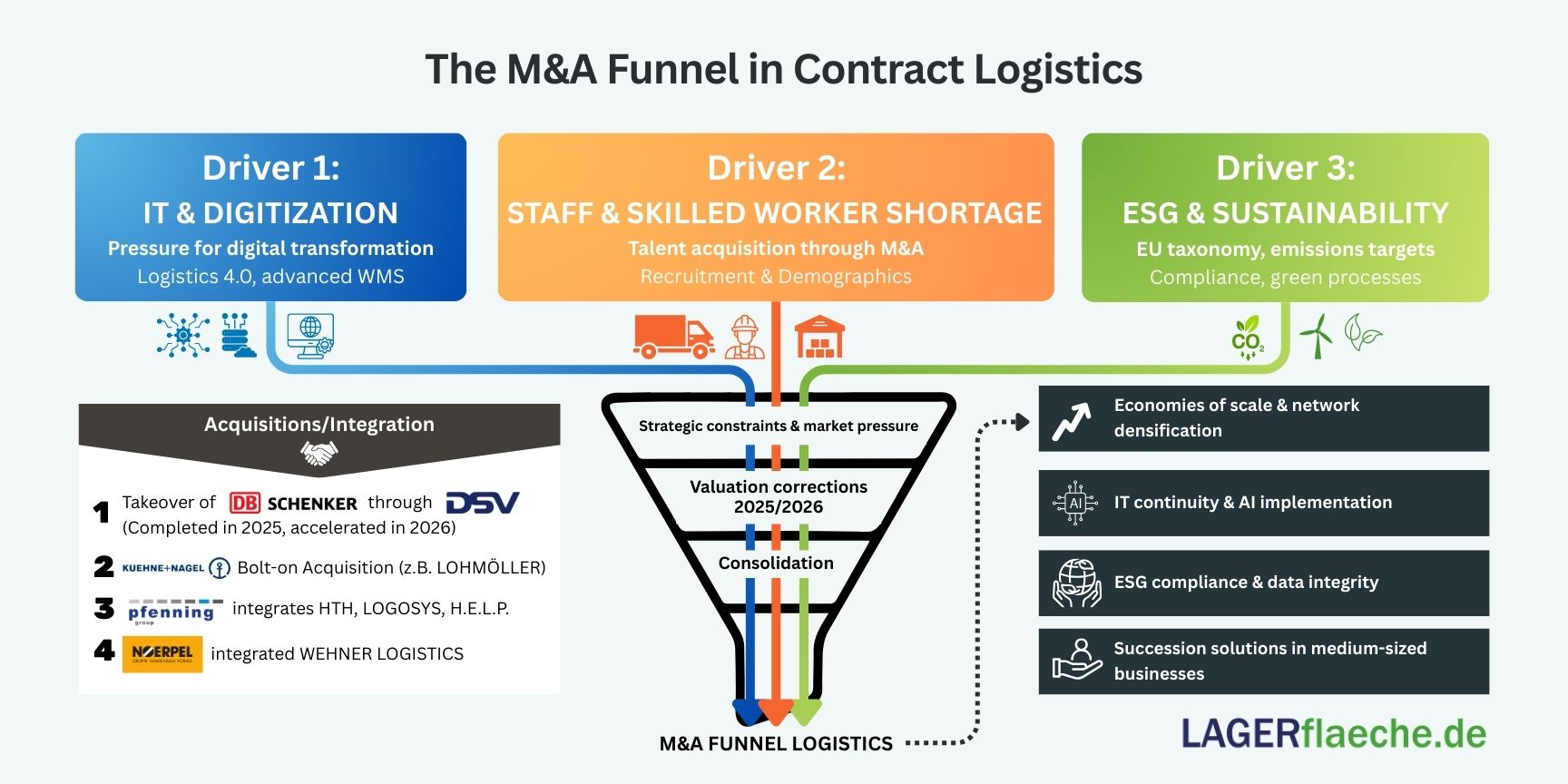

- DSV & DB Schenker: Probably the most spectacular deal in logistics history has been completed. Schenker has officially been part of DSV since May 2025. In February 2026, DSV announced that it would significantly accelerate the integration. The goal is now to complete the process by the end of 2026 – two years earlier than originally planned.

- Kuehne+Nagel: The Swiss giant is continuing its "bolt-on" strategy. In February 2026, the takeover of the road transport activities of the traditional Lohmöller Group was announced in order to further consolidate the European general cargo network.

- pfenning Group: The group has developed into a diversified heavyweight through the integration of Logosys (pharmaceutical logistics), HTH Logistic Solutions (fashion/e-commerce) and H.E.L.P. GmbH (co-packing). Current partnerships, such as with Voith Turbo, show that the focus is now on industrial contract logistics and specialized plant logistics solutions.

- Noerpel & Wehner Logistics: The integration of Wehner (Leverkusen) has been successfully completed. Noerpel is now using this base as a central hub for its Germany-wide e-commerce fulfillment offering.

- SME movements: Companies such as Gräfen Logistik and Gilog (part of the Logosys/pfenning structure) show how specialised units develop more clout under larger roofs.

Term check: Merger, takeover or cooperation?

In reporting, these terms are often used synonymously, but legally and operationally there are worlds in between. This differentiation is essential for specialist portals:

| Feature | Merger | Acquisition | Cooperation (Partnership) |

| Legal entity | Two companies become a new unit. | The buyer swallows the target company. | Both remain legally independent. |

| Control | Joint leadership (theoretical). | Clear hierarchy by the buyer. | Project-related or strategic cooperation. |

| Example | Merger of two equivalent cooperatives. | DSV buys DB Schenker. | General cargo cooperations such as IDS or CargoLine. |

| Risk | Hoch (Kulturclash). | Medium to High (integration costs). | Low (easy to cancel). |

Important question for 2026: Why do we see more acquisitions than cooperations? In times of AI-supported supply chains, loose cooperation is often not enough to ensure the necessary data integrity and IT consistency. Full access to the IT architecture is usually only possible through a takeover.

Was 2025 an exceptional year? A look back from the perspective of 2026

Looking back, 2025 marks the peak of consolidation in Europe. While the years 2021-2023 were characterized by organic growth due to the e-commerce boom, 2025 was the year of inorganic expansion.

Why was 2025 so conspicuous?

- Valuation correction: After the hype of the post-Corona years, company valuations fell to a realistic level in 2024, making 2025 the "buyer's market".

- Interest rate stability: The stabilization of key interest rates gave financial investors and corporations the necessary planning security for billions in investments.

- Domestic focus: Data from 2025 shows that purely domestic deals in Germany increased by over 32%. Companies secured capacities "on their doorstep" to minimize geopolitical risks.

The driving factors: Why the hunger for mergers?

There is no single reason, but a complex web of market pressure and the need to innovate:

- Digital Transformation Pressure & AI

- Small logistics companies cannot afford the millions invested in modern WMS (warehouse management systems) and AI-supported predictive analytics alone. A buyer brings the technology platform; the acquired party provides the physical space and customer proximity.

- Shortage of skilled workers as a reason for acquisition ("acqui-hiring")

- Often a company is not bought because of its trucks, but because of its experienced dispatchers and warehouse clerks. In an empty job market, buying a competitor is the fastest way to recruit.

- ESG (Sustainability) Requirements

- The EU taxonomy requires detailed emissions reports. Large units can finance specialized sustainability teams that prepare this complex data for customers (shippers). Sustainability has gone from being a "nice-to-have" to a hard selection criterion in tenders in 2026.

Change of perspective: What do those involved get out of it?

The Strategic Buyer's Perspective

- Economies of scale: Reduction of unit costs due to higher volume.

- Network density: Closure of white spots (e.g. Kuehne+Nagel's focus on northwestern Germany by Lohmöller).

- Cross-selling: A pharmaceutical customer of Logosys can now be offered the global air freight capacities of the pfenning Group.

The Target's View

- Exit strategy: Solution for succession problems in medium-sized companies. Many owners of the "baby boomer generation" will retire in 2025/2026.

- Investment security: access to capital for warehouse automation (AMRs - Autonomous Mobile Robots).

- Securing survival: Protection against cut-throat competition by belonging to a strong group.

Market impact: What does that do to the competition?

The progressive consolidation leads to an "oligopoly of the mid-level faculty".

- Specialization vs. generalization: While the "big players" such as DSV/Schenker cover standard logistics, highly specialized boutique logistics companies (e.g. for high-tech or dangerous goods) are booming.

- Price development: Contrary to some fears, the mergers have not yet led to massive price jumps, as the efficiency gains (synergies) have to be passed on to customers in part in order to maintain market share.

- Standardization: The power of the big players means that their IT interfaces are becoming the industry standard. Small businesses must adapt to these standards or risk exclusion from digital ecosystems.

International comparison: Germany vs. the world

The German market has caught up massively in the last 12 months, but remains specific.

- USA: "Platform logistics" prevail here. Companies like XPO or GXO act almost like IT companies with connected warehouses. Consolidation is even more advanced there.

- Netherlands & Belgium: Pioneer in the asset-sharing economy. Here, warehouse space is often used across companies – a model that is only now (2026) slowly gaining a foothold in Germany due to data protection concerns.

- Poland & Eastern Europe: Poland has become the No. 1 logistics hub for Western Europe. We are seeing an increase in acquisitions by German companies that are buying nearshoring capacities there.

Country comparison table (M&A activity 2025/26):

| Country | Activity | Main reason |

| Germany | Very high | Succession planning & IT pent-up demand |

| USA | High | Scaling AI platforms |

| Poland | Medium-High | Capacity expansion (nearshoring) |

| France | Medium | Consolidation in the field of food logistics |

Case study: pfenning Group & Logosys – strategy instead of coincidence

A practical example of successful niche consolidation: The challenge: Pharmaceutical logistics places extremely high demands on quality (GDP) and personnel. The deal: The pfenning Group took over Logosys (Darmstadt). The result in 2026: Logosys will continue to act as a centre of excellence for pharmaceuticals within the Group. The pfenning Group was thus able to suddenly expand its portfolio to include high-margin healthcare services without having to laboriously build up the expertise itself. Benefit for the reader: This example shows that takeovers today are often skills purchases, not pure capacity purchases.

Conclusion: Strategic questions for logistics decision-makers in 2026

Anyone working in contract logistics today must ask themselves three questions:

- Am I a hunter or the hunted? Those who do not actively grow will come under pressure in the long term due to the rising fixed costs for IT and ESG.

- How deep is my IT integration? In 2026, the logistics software will be the centerpiece, the warehouse will only be the body.

- Do I have a niche? Only those who are either "huge" or "highly specialized" will survive in the new market structure.

Forecast: The really big megadeals have been concluded for the time being. The year 2026 and 2027 will be characterized by "bolt-on" acquisitions – small, strategically valuable acquisitions that perfectly complement existing networks.

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Live Cargo: Logistics, Collection Points and Value-added Services for Animal Transport

You can't store animals on pallets—so how does the supply chain for live cargo actually work? Discover the strict laws, Value Added Services, and specialized logistics hubs of animal transport in our comprehensive international overview....

CSRD-compliant: What tenants (must) demand from their logistics property now

Is your warehouse becoming an ESG black box? Discover our tenant checklist and learn exactly which data you must demand from your landlord for your CSRD reporting right now....

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....