digital dashboards floating over pallet spaces displaying dynamic pricing tags like Pay-per-Pallet and Fixed Rent.")

The New Logic of Warehouse Contracts: Fixed Rent, Flex Model or Pay-per-pallet

Table of Contents

- The Logistical Trilemma: Which Inventory Pricing Models Dominate the Market?

- Fixed Contracts in the Endurance Test: When is Rigidity an Economic Advantage?

- Variable Pricing: The Mathematical Reality Behind Pay-per-Pallet

- The Small Print: Top Surcharges and Seasonal Dynamics

- Protection for the service provider: clauses on minimum occupancy

- Operational Risk Distribution: Who Bears the Costs of Inefficiency?

- Inventory Procurement and Search Intelligence: International Comparison

- Practical Example: The Transformation of MedTec GmbH

- Frequently Asked Questions (FAQs) – Intelligently Answered

- Conclusion and Checklist for Practice: The Way to the Optimal Storage Contract

The global logistics landscape is undergoing rapid structural change. Driven by volatile supply chains, the ongoing e-commerce boom and the need for maximum capital efficiency, logistics managers and supply chain managers are faced with a central question: What does the economically optimal structure of a modern warehouse contract look like? For a long time, the classic fixed rent dominated. But rigid capacities quickly become a yield killer in a world characterized by unpredictable market and demand fluctuations. On the other hand, highly flexible models carry hidden risks and complex price clauses. What logic prevails? This guide analyzes the common pricing models in detail, sheds light on operational risk distributions, shows international differences in warehouse procurement and provides you with concrete tools for your next contract negotiation.

The Logistical Trilemma: Which Inventory Pricing Models Dominate the Market?

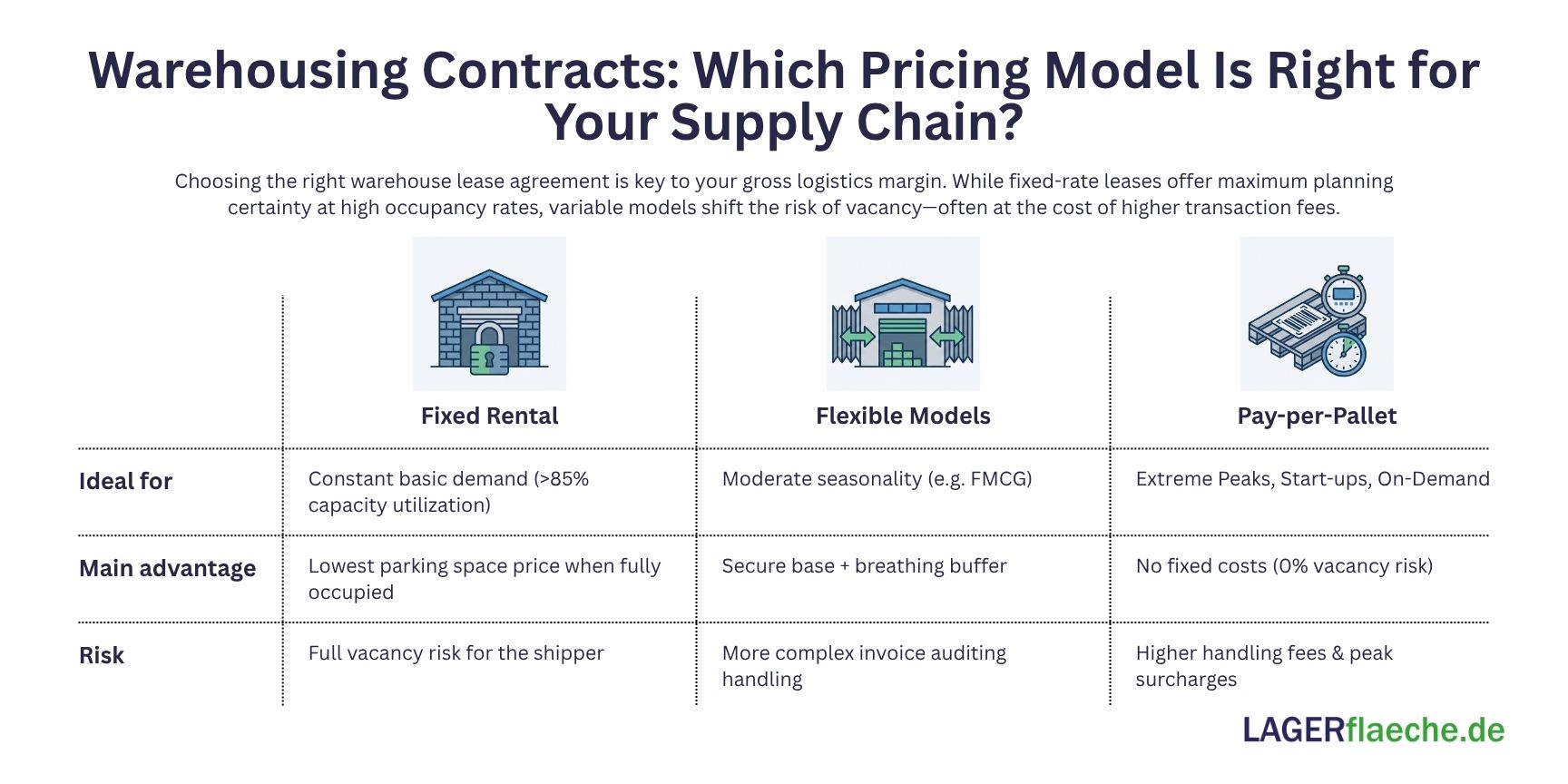

Anyone who procures storage capacities today no longer chooses just a property, but a financial mathematical model. Basically, three primary billing logics have established themselves on the market, each of which has specific risk and opportunity profiles.

The Fixed Rent (Fixed-rate Model)

The classic fixed rent is based on the long-term provision of a defined area (in square meters) or a fixed number of pallet spaces. The user pays a fixed amount – regardless of whether the warehouse is at 100% capacity or empty.

The Flex Model (Hybrid Model)

This model combines a fixed basic component with a variable component. For example, the shipper rents a base area for 60% of its average demand at a low fixed price. If the volume exceeds this limit, additional space or parking spaces are billed at a higher, flexible daily rate on a daily or weekly basis.

The Pay-per-pallet Model (Activity-Based Pricing)

This is a purely transaction-based model. There are (theoretically) no fixed rental costs. Exactly the number of pallets stored per day or week is paid, often linked to the operational handling costs (inbound/outbound). This model is strongly driven by on-demand logistics platforms.

Fixed Contracts in the Endurance Test: When is Rigidity an Economic Advantage?

In times of agile management methods, fixed rent is often criticized as outdated. But this view does not go far enough. For companies with highly stable, predictable shipment flows and low seasonality (e.g. in the chemical industry or consumer staples), the fixed contract remains the economic anchor.

The biggest advantage lies in the strongly degressive economies of scale. While the price per pallet space is linear or even progressive over the entire term of flexible models, the average costs per unit fall massively with increasing capacity utilization in fixed contracts.

Key figure from practice: With a capacity utilization rate of over 85%, a fixed contract is usually 12 to 18% cheaper than a comparable pay-per-pallet model, as the logistics service provider (3PL) does not have to price in vacancy risk.

In addition, fixed contracts (often with terms of 3 to 5 years) ensure that companies have access to scarce logistics space in top locations (e.g. around Frankfurt or Hamburg). The disadvantage: If the occupancy rate falls below 70% due to market slumps, the fixed rent mutates into a massive burden on the gross margin.

Variable Pricing: The Mathematical Reality Behind Pay-per-Pallet

The promise of pay-per-pallet sounds tempting: "We breathe with your business." However, pricing in the variable model follows a tough logistical calculation. No 3PL (Third-Party Logistics Provider) can afford to leave space permanently unused without charging a premium.

The price structure of pay-per-pallet is usually divided into two dimensions:

- Storage Fee: Cost per pallet per day/week.

- Handling fee: Cost per movement (also known as in/out fee).

For the profitability calculation, the inventory turnover is the decisive variable.

Inventory Turnover = Cost of Goods Sold / Average Inventory Value

A calculation example illustrates the risk: With an extremely low turnover rate (slow-moving), the daily variable storage fees quickly eat up the margin advantage of the flexible model. Conversely, very high turnover with low inventories leads to extreme handling costs, which are often priced significantly higher in the variable model than in the fixed contract.

The Small Print: Top Surcharges and Seasonal Dynamics

A common fallacy with flex models is the assumption that additional capacities are available indefinitely and under the same conditions during the peak season. Peak season surcharges have therefore become established in modern logistics contracts.

Especially in the e-commerce environment (Black Friday, Christmas business), the demands on warehouse staff and infrastructure are increasing drastically. Service providers protect themselves in the contracts through the following mechanisms:

Progressive graduation: Up to a capacity utilization of 110% of the base volume, the standard flex price applies. Between 110% and 130%, a surcharge of 25% on the pallet price, for example, applies.

Capacity cap: The service provider only guarantees flexibility up to a hard upper limit. Everything beyond that must be requested on a case-by-case basis and negotiated on a daily basis.

If you don't negotiate these clauses precisely, you'll be in for a nasty surprise in the fourth quarter, which can completely nullify the annual logistics cost efficiency.

Protection for the Service Provider: Clauses on Minimum Occupancy

Why do logistics service providers agree to highly variable contracts in the first place? The answer is that they rarely do it without a safety net. This is where Minimum Volume Commitments (MVC) clauses come into play.

These clauses form the legal and economic foundation for cushioning the investment risk of the service provider (e.g. in racking systems, IT interfaces or industrial trucks).

How it works: The shipper agrees on a pay-per-pallet model, but contractually undertakes to pay for an occupancy of at least 2,000 pallet spaces on a monthly average, for example.

The consequence: If the actual stock falls to 1,200 pallets, the service provider still charges for the agreed 2,000 spaces (so-called phantom pallets).

For the buyer, this means that a supposedly pure pay-per-pallet model turns out to be a disguised fixed contract on closer inspection in the lower volume range.

Operational Risk Distribution: Who Bears the Costs of Inefficiency?

A storage contract not only regulates prices, but primarily the distribution of operational risks. When choosing the contract model, these risks shift fundamentally between the shipper and the service provider:

| Risk type | Fixed Rent (Shipper Risk) | Pay-per-Pallet (Service Provider Risk) |

| Vacancy risk | It is 100% up to the shipper. | Lies with the service provider; he has to find third-party customers. |

| Productivity risk | Service provider optimizes internally to maximize margin. | Higher risk for service providers; slow processes reduce throughput. |

| Space efficiency | Shipper pays; how tightly he packs is his lever. | Service provider tries to make optimal use of heights (volume optimization). |

| Staffing | Fixed cost structures often rigidly coupled. | Service providers have to manage personnel extremely flexibly. |

A critical issue in flexible contracts is the risk of blocking. If the shipper delivers inferior pallets or the notification data is inaccurate, the service provider's operational process comes to a standstill. As a result, service level agreements (SLAs) are increasingly being found in modern contracts, which directly impose penalties or special fees on the part of the shipper for inefficiencies (e.g. waiting times for trucks, delayed data transmission).

Inventory Procurement and Search Intelligence: International Comparison

The procurement of storage space and the enforcement of certain contractual logics is not a purely business-related issue, but a strongly geographical and cultural one. Anyone who manages pan-European or global supply chains will find that the "standard" contract models differ drastically.

Germany: The Benchmark of Rigidity

In Germany, the long-term contract logistics contract continues to dominate, with a strong tendency towards fixed rents or very conservative hybrid models. The reason for this is the extreme shortage of space in the prime markets (front-runners such as Munich, Frankfurt, Stuttgart) and the risk-averse financing structure of German logistics real estate developers. Banks usually require long-term leases (7 to 10 years) with tenants with strong credit ratings for the financing of logistics halls. Pure pay-per-pallet models without hard minimum occupancy are hardly feasible in Germany in the first-class segment (A-locations) apart from pure multi-user facilities.

United Kingdom (UK): Pioneering Flexibility and Search Intelligence

The British market is much more agile compared to Germany. Driven by the extremely high share of e-commerce (approx. 26-28% of the total retail trade) and the disruptions of Brexit, marketplace-based warehousing-on-demand models have established themselves here. Search intelligence platforms convey free capacities in real time. Pay-per-pallet is a standard financial product in logistics in the UK. Contracts are often much shorter (12 to 24 months), and the willingness of service providers to take on speculative volume risk is significantly higher than in continental Europe.

Central and Eastern Europe (CEE – Poland, Czech Republic, Romania): The Growth Market in Upheaval

In countries such as Poland (especially around Łódź and Warsaw) or the Czech Republic, the situation is twofold. Due to the massive influx of nearshoring projects (relocation of production away from Asia closer to Europe), huge logistics parks are being built. Large-scale fixed-term leases dominate here, as international corporations set up their central European distribution centers (EDCs) there. At the same time, prices per square meter are often 30 to 50% cheaper than in Germany. As a result, shippers in CEE are more willing to accept the vacancy risk of a fixed contract because the absolute costs per square meter are less of a burden on the overall balance sheet.

The USA: The Realm of "Third-party Marketing" and Standardized Contracts

Globally, the USA shows where the journey is heading. Due to the sheer size of the market and the standardization of logistics halls (cross-docking structures), the fungibility of warehouse space is extremely high. Search intelligence here means the use of AI-supported algorithms that match freight flows with free pallet spaces on a daily basis. Pure pay-per-pallet models are firmly anchored in the market there, as the secondary market for the re-letting of blocked space is extremely liquid.

Practical Example: The Transformation of MedTec GmbH

To make the theoretical models tangible, let's look at the fictitious (but based on real project data) MedTec GmbH, a medium-sized manufacturer of medical consumables.

The initial situation

MedTec GmbH recorded a strong seasonal business (high demand in autumn/winter, summer slump). It operated a rented permanent warehouse with 10,000 pallet spaces at a fixed cost of €60,000 per month (€6.00 per space, regardless of occupancy), excluding staff.

The reality: In winter, the warehouse was at 100% capacity, in the summer months the capacity utilization dropped to 4,500 pallets. The effective costs per pallet space used rose mathematically to a dramatic €13.33 in the summer.

The restructuring of the warehouse contract

The company restructured the contract into a hybrid flex model in collaboration with a modern 3PL service provider:

- Fixed core: 5,000 pallet spaces were blocked as fixed rents – but at a negotiated preferential price of € 5.00 per space (= € 25,000 fixed costs).

- Flexible shell: Everything over 5,000 pallets was billed in the pay-per-pallet model, at a rate of €0.28 per pallet per day (equivalent to approx. €8.40 per month when fully used).

The economic result

The annual average occupancy was 7,200 pallets.

The savings: MedTec GmbH reduced its pure storage costs by €198,240 per year (approx. 27.5%) and completely eliminated the financial risk of summer vacancy without risking supply bottlenecks during the peak season.

Frequently Asked Questions (FAQs) – Intelligently Answered

Question: When is pay-per-pallet worthwhile over a fixed rent?

Answer: Pay-per-pallet is primarily worthwhile if there is a turnover frequency of more than 6 to 8 times per year, strong seasonal volume fluctuations (amplitudes of over 30%) and if no specialized infrastructure (e.g. refrigeration, hazardous goods) is required.

Question: How high are the usual peak surcharges in contract logistics?

Answer: In European metropolitan areas, peak season surcharges range from 15% to 35% of the basic pallet tariff, usually limited to the period from October 15 to December 31.

Question: Why do logistics service providers demand a minimum occupancy despite the flex model?

Answer: Because the service provider has fixed costs for real estate leasing, hall investments (CapEx) and permanent core staff. The minimum occupancy (MVC) secures its fundamental contribution margin.

Question: How does search intelligence influence warehouse procurement in Europe?

Answer: Digital platforms and AI-supported search intelligence now make it possible to compare free capacities in real time across national borders. As a result, the traditional, purely regional relationship business is breaking up, and spot market prices for pallet spaces are becoming more transparent.

Conclusion and Checklist for Practice: The Way to the Optimal Storage Contract

The "new logic" of storage contracts is not a farewell to fixed rents, but a plea for mathematical precision. The optimal model is almost always a hybrid flex model that is precisely calibrated to the historical standard deviation of your inventory data.

Your checklist for the next contract negotiation:

Conclusion: Anyone who negotiates contracts today must think logistics and financial mathematics together. This is the only way to turn the warehouse from a cost block into a strategic flexibility advantage.

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Live Cargo: Logistics, Collection Points and Value-added Services for Animal Transport

You can't store animals on pallets—so how does the supply chain for live cargo actually work? Discover the strict laws, Value Added Services, and specialized logistics hubs of animal transport in our comprehensive international overview....

CSRD-compliant: What tenants (must) demand from their logistics property now

Is your warehouse becoming an ESG black box? Discover our tenant checklist and learn exactly which data you must demand from your landlord for your CSRD reporting right now....

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....