Material Shortage 2.0: Why the Supply Crisis is Returning and How Logistics Must Act Now

Table of Contents

- Status Quo: Is the Shortage of Materials the New "Normal"?

- Impact on Logistics: The End of "Just-in-Time"?

- Focus on Germany: Why are we being Hit Harder?

- The European Comparison: Poland and France

- Global Discrepancies: USA and China

- Analysis of Critical Product Groups: Where is the Biggest Problem?

- Practical case study: "Maschinenbau Müller GmbH"

- Solutions: Strategies for Purchasing and Logistics

- Conclusion: Logistics is Becoming a Strategic Competitive Factor

Global supply chains are not coming to rest. Anyone who thought that "just-in-time" normality would return after the pandemic is mistaken. The industry is facing a new wave of material shortages – but this time the causes are more complex and the regional differences more serious. For logistics decision-makers and buyers, the question is no longer whether a delivery arrives late, but how to manage volatility profitably.

In this technical article, we analyze the current situation of the raw material supply, shed light on the drastic differences between Germany, Europe and the world market, and provide tangible strategies for resilient logistics.

Status Quo: Is the Shortage of Materials the New "Normal"?

Why does the chain keep breaking off? It is a toxic mix of geopolitical tensions, protectionist trade barriers and climate change that makes transport routes impassable.

Current data from the ifo Institute show that in German core industries (mechanical engineering, automotive, electrical) more than 40% of companies are again complaining about serious bottlenecks in intermediate products [source: ifo Business Surveys]. But unlike in 2021, the problem is often not with production, but with availability at the right time in the right place.

Important questions that we answer here:

- Are the warehouses empty or are the goods stuck in traffic jams?

- Which raw materials are the current "pain points" of the industry?

There is a shift: While semiconductors continue to be in short supply, basic materials such as special steels, plastics (due to oil price fluctuations) and rare earths are now also coming into focus. For logistics, this means that the planning effort is exploding.

Impact on Logistics: The End of "Just-in-Time"?

The shortage of materials is forcing a paradigm shift in logistics strategy. "Just-in-time" (JIT), which has been optimized for decades, is increasingly giving way to "just-in-case" (JIC). But this change is expensive.

The bullwhip effect in full force

Small fluctuations in demand from the end customer lead to massive overorders along the chain due to the fear of shortages.

- As a result, logistics service providers suddenly have to buffer huge quantities, followed by phases of standstill.

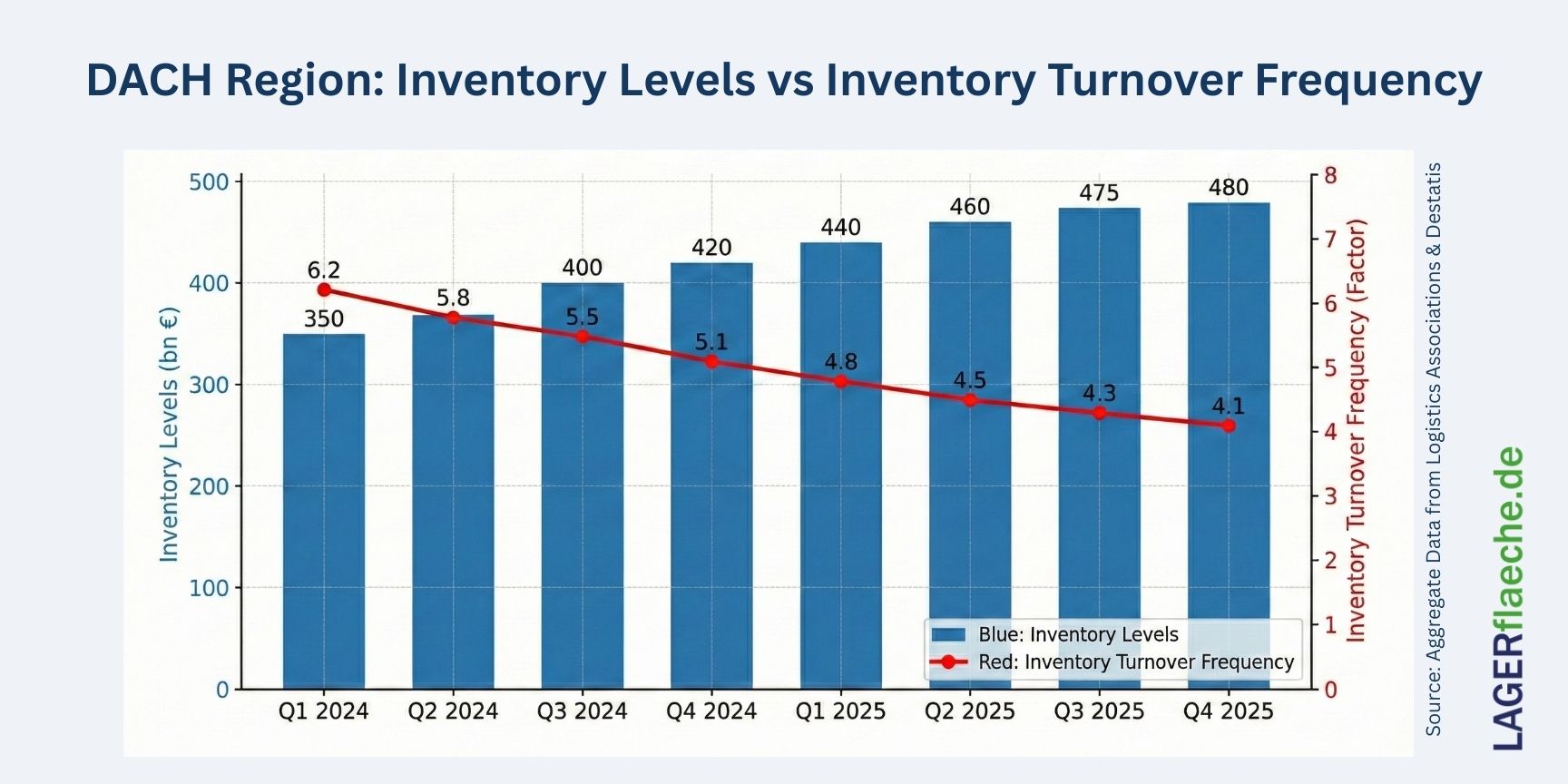

- Cost trap warehousing: According to current surveys by the BME (Federal Association for Materials Management, Purchasing and Logistics), warehousing costs have risen by an average of 12-15% compared to the previous year.

Modal Shift: When the ship is too slow

Due to a lack of materials, express transports by air freight often have to be organized to prevent line downtimes. This drives up the CO2 balance and freight costs and thwarts sustainability goals.

Focus on Germany: Why are we being Hit Harder?

Germany, as the "workbench of Europe", is suffering disproportionately from the current shortage of materials. Why is that?

- High export dependence and complexity: German products (cars, machines) are highly complex. If a single screw or chip is missing, the finished product worth tens of thousands of euros is in stockpile.

- Energy-intensive intermediate products: High energy prices in Germany have led to a reduction in domestic production of intermediate products (e.g. aluminium, ammonia for chemicals). They are now more dependent on imports – and thus on logistics.

- Infrastructure deficits: Dilapidated bridges and an overloaded rail network make it difficult to transport the few available materials internally.

A report by the DIHK warns: "De-industrialization begins with the intermediate products." If raw materials are no longer produced in NRW or Bavaria, the supply chain will be extended by thousands of kilometers.

The European Comparison: Poland and France

Not all European countries are affected equally. A look beyond the borders shows different strategies and effects.

Poland: The winner of nearshoring?

Poland has established itself as a logistics hub. Many German companies are relocating storage capacities to the Vistula River.

- Advantage: Shorter distances to Eastern Europe and a growing port capacity (Gdansk).

- Problem: Here, too, the shortage of skilled workers in logistics (truck drivers) is increasing, which slows down the flow of materials, even if goods were there.

France: Energy as an anchor of stability

France benefits from cheaper industrial electricity through nuclear energy in material production (e.g. aluminium smelters). The dependence on imported intermediate products in the energy sector is lower than in Germany. This currently makes French supply chains somewhat more resilient to price shocks for materials that are energy-intensive to produce.

Global Discrepancies: USA and China

When we leave the European continent, we see that material shortages are often politically driven.

USA: The "Inflation Reduction Act" (IRA) as a magnet

The USA is luring production capacities into its own country with massive subsidies (IRA).

- Logistics effect: The "reshoring" initiative shortens intra-American supply chains. U.S. companies often have better access to steel and building materials as domestic production ramps up. For European buyers, this means that US materials are becoming more expensive or are blocked for export ("America First").

China: Control of the mine

According to the International Energy Agency (IEA), China controls the processing of about 60-70% of the world's critical minerals (lithium, cobalt).

- The risk: China uses export restrictions (as was recently the case with gallium and germanium) as a geopolitical bargaining chip.

- Impact: While Chinese factories are supplied, European logistics companies are waiting for clearance in the ports of Shanghai or Ningbo.

Analysis of Critical Product Groups: Where is the Biggest Problem?

In order to adapt logistics, we need to know what is missing.

Semiconductors & Electronics

Despite new factories, the situation remains tense for older chip generations (important for industry and automotive). The "allocation" determines the market. Logistics companies have to react extremely flexibly to short-term delivery windows.

Building Materials & Steel

Here, it is not physical scarcity that is the main problem, but volatility. Steel mills spontaneously shut down production when energy prices are high. The result: sudden supply leaks in construction and mechanical engineering logistics.

Chemical raw materials

There is a real shortage here in Germany due to production migration. Imports from Asia or the USA require special hazardous goods logistics and tank containers, which are in short supply worldwide.

Practical case study: "Maschinenbau Müller GmbH"

Note: This example is fictitious, but derived from real-world market scenarios.

The initial situation:

A medium-sized mechanical engineering company from Baden-Württemberg (turnover €150 million) obtains special castings from China and electronic controls from Germany.

The problem:

- The Chinese supplier has to cut production due to electricity rationing (material is missing).

- The German electronics supplier has no chips.

The impact on logistics:

The warehouse for semi-finished goods is full. Unfinished machines worth €10 million are blocking the assembly halls. Liquidity is falling.

The solution (best practice):

- Strategic warehouse: The company rented external warehouse space to outsource the unfinished machines (cost increase, but cash flow protection through partial invoicing where possible).

- Dual Sourcing & Nearshoring: A new supplier of castings in Turkey has been qualified. The transport time was reduced from 6 weeks (sea) to 5 days (truck).

- AI-powered forecasting: Introduction of a tool that no longer calculates delivery times statically, but based on real-time risk data (port strikes, weather).

Solutions: Strategies for Purchasing and Logistics

What can companies do to avoid remaining at the mercy of the markets?

- Increased transparency (Tier N monitoring): It is not enough to know the direct supplier. You have to know where its raw materials come from. Digital twins of the supply chain help to identify risks at an early stage.

- Rethinking inventory management: Safety stocks must be dynamically adapted to the world situation. The safety stock formula must include external risk indicators.

- Diversification of transport routes: Those who rely only on sea freight lose out in port congestion. A multimodal strategy (combination of rail, such as the "New Silk Road", and sea/air) is mandatory.

- Closer collaboration: Logistics, purchasing and production must no longer be silos. Sales and Operations Planning (S&OP) must take place weekly to synchronize material flow and production schedule.

Conclusion: Logistics is Becoming a Strategic Competitive Factor

The shortage of materials is not a temporary phenomenon, but a symptom of a deglobalizing world economy. Countries like Germany have to radically change their procurement strategies in order to remain competitive. A comparison with the USA and China shows that those who control the raw materials or have short distances win.

For logistics, this means moving away from pure cost optimization and towards resilience. The ability to restructure supply chains within days in the event of material failure is the new currency in international competition.

References:

- Ifo Institute for Economic Research: Business Surveys 2024/2025.

- BME (Federal Association for Materials Management, Purchasing and Logistics): Top key figures in purchasing.

- Destatis (Federal Statistical Office): Producer price indices of industrial products.

- DIHK: Report on the raw material situation of German industry.

- International Energy Agency (IEA): Critical Minerals Market Review.

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Live Cargo: Logistics, Collection Points and Value-added Services for Animal Transport

You can't store animals on pallets—so how does the supply chain for live cargo actually work? Discover the strict laws, Value Added Services, and specialized logistics hubs of animal transport in our comprehensive international overview....

CSRD-compliant: What tenants (must) demand from their logistics property now

Is your warehouse becoming an ESG black box? Discover our tenant checklist and learn exactly which data you must demand from your landlord for your CSRD reporting right now....

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....