Logistics Real Estate 2026: Between Resilience and Realignment – An In-Depth Analysis

Table of Contents

- Status Quo Germany: Vacancies and Take-up at the End of 2025

- The "Gray Vacancy": The Hidden Burden of Contract Logistics Companies

- Regional Analysis: Where is the Vacancy Rate Highest?

- Root Cause Research: Why is the Market Breathing so Hard at the Moment?

- Forecast 2026 and 2027: When will the Rebound Come?

- Europe in Comparison: Germany vs. Poland vs. UK

- Global View: US Resilience and the China Dilemma

- Practical Check: What does this Mean for You?

- Important Questions for the Market:

- Conclusion

It's January 2026. The past year 2025 marked a turning point for the German and global logistics industry. While the years after the pandemic were marked by extreme space shortages, the tide has turned. We are looking at a market that is more differentiated than ever before. For contract logistics companies, project developers and portfolio holders, the central question is: Is the current vacancy rate a warning signal or the necessary market shakeout for the next upswing?

In this technical article, we examine the figures for the end of 2025, analyze the causes of vacancies and venture a well-founded forecast for 2026 and 2027.

Status Quo Germany: Vacancies and Take-up at the End of 2025

The German market for industrial and logistics real estate closed 2025 with a remarkable stabilization. According to current data from Colliers (January 2026), take-up of around 5.9 million m² was achieved nationwide – a moderate increase of around 4% compared to the previous year.

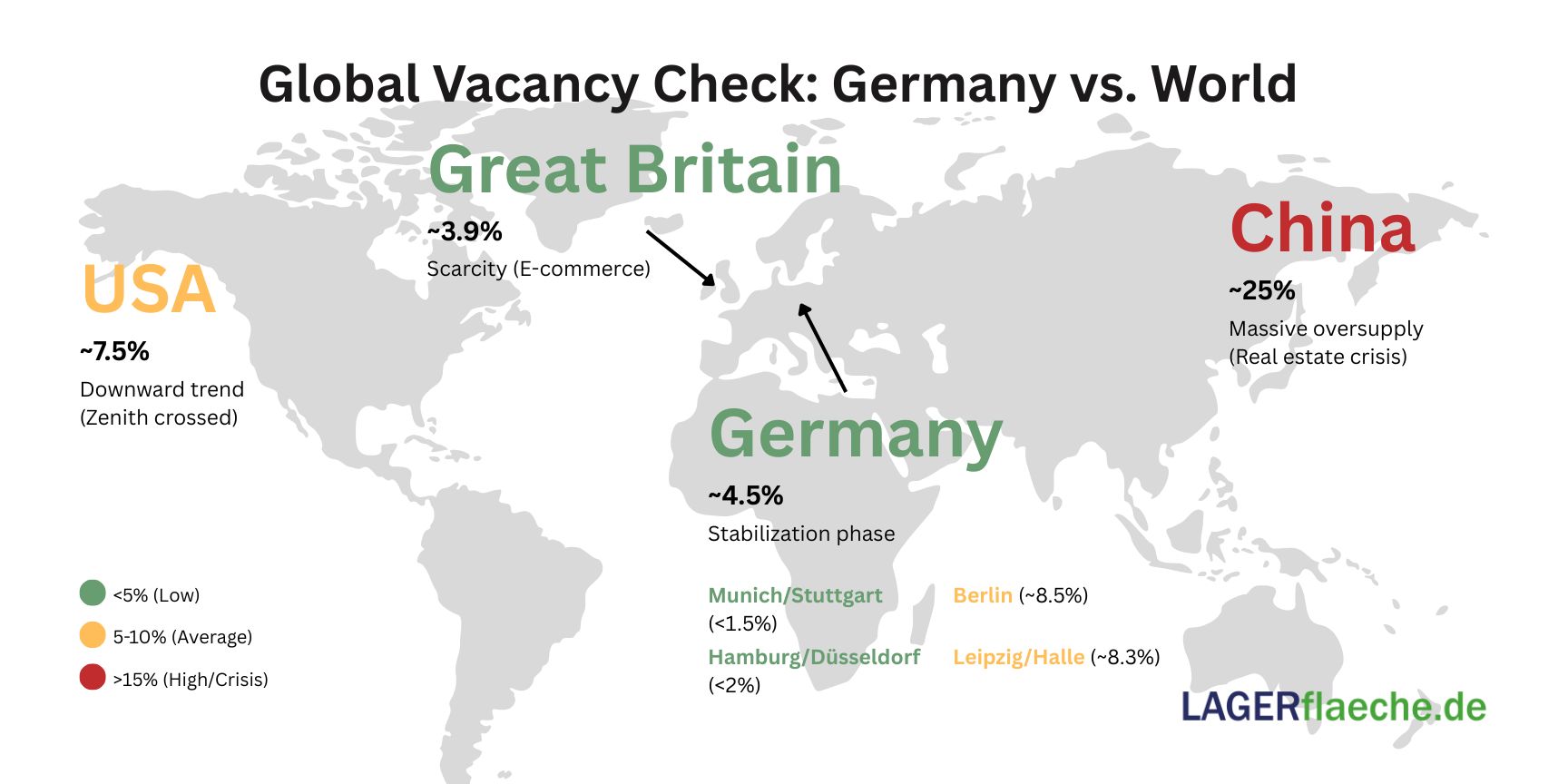

Nevertheless, the vacancy rate for so-called "big box" properties (areas > 10,000 m²) has risen slightly and is now around 4.3% to 4.5% nationwide (source: CBRE/Colliers). By comparison, in the boom years of 2021/2022, this figure was often below 2%.

The key question: Why is the vacancy rate rising despite growing take-up?

The answer lies in the type of surfaces. While modern A-location properties are absorbed immediately, speculative new buildings in B- and C-locations as well as energy-efficient outdated existing properties linger longer on the market.

The "Gray Vacancy": The Hidden Burden of Contract Logistics Companies

For professionals in the niche, the official vacancy rate is only half the story. Much more critical is the "gray vacancy" at the end of 2025. This refers to space that is permanently let, but whose pallet spaces are empty due to falling order volumes or more efficient inventory management.

- Subletting as a trend: In top markets such as Frankfurt am Main, subletting already accounted for 23% of total take-up at the end of 2025 (source: Realogis/Konii).

- Margin pressure: Contract logistics companies (3PLs) that have rented space at high prices are struggling with the fixed cost burden of empty shelf meters. Many are now offering these capacities on spot market platforms at short notice, which is putting pressure on the classic rental market.

Regional Analysis: Where is the Vacancy Rate Highest?

The gap between the regions has widened massively in 2025. We see a clear division of Germany:

| Region | Vacancy rate (end of 2025) | Trend |

| Munich / Stuttgart | < 1.5% | Chronic scarcity |

| Hamburg / Düsseldorf | ~ 2.0 % | Stable |

| Berlin | ~ 8.5 % | High supply surplus due to new construction |

| Leipzig / Halle | ~ 8.3 % | Consolidation phase after boom |

Why Berlin and Leipzig? In these regions, massive speculative land was completed in 2023 and 2024. As the e-commerce sector has normalized its pace of expansion, these spaces are now meeting more cautious demand.

Root Cause Research: Why is the Market Breathing so Hard at the Moment?

The reasons for the empty parking spaces are complex and go beyond the pure economic weakness:

- Nearshoring & Friendshoring: Companies are relocating production and warehousing back to Europe. However, this process is lengthy. The areas are being secured, but not yet fully equipped.

- Inventory optimization through AI: Thanks to advanced forecasting tools, retailers now need up to 15% less safety stock than they did in 2023. This leads to free capacity on the shelves.

- ESG obsolescence: Properties that do not meet the latest sustainability standards (solar obligation, heat pumps) fall out of the grid of major tenants. This "structural vacancy" is difficult to remedy.

- Interest rate turnaround aftermath: The high financing costs of previous years have stopped many owner-occupier projects, which means that companies are increasingly pushing into rent, but are looking for smaller, more efficient units there.

Forecast 2026 and 2027: When will the Rebound Come?

The "logistics experts" and institutes such as the BALM (Federal Office for Logistics and Mobility) predict a gradual recovery for 2026.

- 2026: It is expected to see real growth in logistics output of approx. 0.5 % to 1.1 %. The vacancy rate will stabilize as hardly any speculative new buildings come onto the market (construction starts in 2024 were at a record low).

- 2027: Experts expect a shortage here. Since the share of new construction has already fallen to below 50% of take-up in 2025 (source: CBRE), rising demand (driven by the recovery of industry) will meet very limited supply. Rising rents from mid-2027 are almost certain.

Europe in Comparison: Germany vs. Poland vs. UK

Germany remains the anchor point, but the momentum is shifting:

- Poland & CEE: Here, vacancy rates are often higher (up to 8%), but the absorption rate is enormously high due to nearshoring effects from Western Europe. Poland is the winner of de-globalization.

- Great Britain: A very mature market. Vacancies are already falling below 4% again, as the e-commerce share there remains the global leader with a projected 27% by 2029 (source: Savills/Catella).

- France: Similar to Germany, but with a stronger focus on urban logistics in the Paris region.

Global View: US Resilience and the China Dilemma

The comparison to the global giants is crucial for investors:

- USA: According to Prologis (Bold Predictions 2026), the vacancy rate peaked at 8.5% in Q3 2025 and is now already falling back towards 7%. The US market reacts faster and more volatile than the European market.

- China: There is a real estate crisis here. In Tier 1 cities, vacancy rates are as high as 25% in some cases (source: Savills/CBRE China). A massive oversupply meets weakening domestic demand. This depresses the global return expectations of international portfolio managers.

Practical Check: What does this Mean for You?

For owners: Invest in ESG. A building without a photovoltaic system and state-of-the-art insulation will be considered a "stranded asset" in 2027. Tenants are willing to pay higher rents for energy efficiency in order to save on utility costs.

For contract logistics companies: Use the current market phase to secure long-term contracts or negotiate flexibility clauses for "grey vacancy". Cooperation with marketplaces for warehouse space can help to smooth out occupancy.

For project developers: The focus is shifting from greenfield sites to brownfields and multi-level logistics in urban areas.

Important Questions for the Market:

- Have we built too much or just in the wrong place?

- How much of the current vacancy is actually "ESG-related" and therefore no longer rentable?

- When will the increase in efficiency through AI compensate for the space required for nearshoring?

Conclusion

The end of 2025 was the year of the correction. 2026 will be the year of efficiency. Those who see their empty pallet spaces as an opportunity for digitization and ESG compliance will be among the winners in 2027 when the shortage of space in the top locations strikes again.

Would you like a detailed evaluation for a specific logistics region or do you need a calculation aid for the economic efficiency of photovoltaic retrofits on existing areas?

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Live Cargo: Logistics, Collection Points and Value-added Services for Animal Transport

You can't store animals on pallets—so how does the supply chain for live cargo actually work? Discover the strict laws, Value Added Services, and specialized logistics hubs of animal transport in our comprehensive international overview....

CSRD-compliant: What tenants (must) demand from their logistics property now

Is your warehouse becoming an ESG black box? Discover our tenant checklist and learn exactly which data you must demand from your landlord for your CSRD reporting right now....

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....