, with robots and digital networking.")

The Future of Logistics is Now – Welcome to the Era of Neo-Logistics

Table of Contents

- What is "Neo-Logistics"? The End of the Reactive Chain

- The Real Driver: How the Consumer is Turning Logistics Upside Down

- Big Players vs. SMEs: Who will Win the Race?

- The New Power of Data: What's Changing for the Shipper

- Practical Example: Contract Logistics Company "Müller & Partner" (hypothetical)

- Green Logistics: From a Fig Leaf to a Tough Competitive Factor

- Global Competition: Why Germany's Logistics Industry needs to Wake Up

- Conclusion and Outlook: Logistics is Dead – Long Live Neo-Logistics

The logistics industry is at a turning point. After years of optimization as part of "Logistics 4.0" – the digitization of existing processes – we are now entering a new phase: neo-logistics. But is this term just another buzzword or does it describe a fundamental revolution in the global flow of goods?

The answer is clear: it's a revolution. Driven by exponential data growth, artificial intelligence, radically changed customer expectations and irreversible ecological pressure, tomorrow's logistics will not only be more efficient, but fundamentally different. It will be proactive, autonomous, hyper-connected and imperatively sustainable.

For a specialist portal like ours, the question is not whether, but how quickly the players have to adapt. Who are the winners and losers in this change? What does this mean in concrete terms for freight forwarders, contract logistics companies and shippers in Germany in a global comparison? This article dives deep into the mechanisms of neo-logistics.

What is "Neo-Logistics"? The End of the Reactive Chain

Logistics 4.0 was digitalization. We have collected telematics data, implemented transport management systems (TMS) and warehouse management systems (WMS). Neo-Logistik goes the decisive step further: it uses this data not only for description, but also for prediction and autonomous control.

Neo-Logistics is:

- Hyper-connected: Not only the truck is connected, but every pallet, every package, every machine. The Internet of Things (IoT) provides a constant stream of data.

- AI-driven: Instead of a dispatcher planning routes, AI dynamically optimizes thousands of variables in real time – from weather data to traffic to machine failures.

- Platform-based: Open ecosystems and digital platforms are replacing rigid, bilateral connections. Cargo space is traded like on a stock exchange, capacities are shared (keyword "Physical Internet").

- Resilient and transparent: Through total networking (e.g. via blockchain for tamper-proof data), the supply chain becomes "transparent" and can proactively react to disruptions (such as the Suez Canal blockade or pandemics).

So the key question is no longer: "Where is my shipment?", but: "What disruption will affect my shipment in 36 hours, and what alternative route has the AI already booked?"

The Real Driver: How the Consumer is Turning Logistics Upside Down

The biggest disruptor in logistics is not based in Silicon Valley, it sits on the sofa at home: the consumer. The "Amazonization" of expectations has brutally shifted the bar for all areas of logistics – B2B and B2C.

- Speed: "Next Day" is standard, "Same Day" (Instant Delivery) becomes the differentiating feature. According to a study by Capgemini (2023), 55% of consumers are willing to switch to a competitor that offers faster deliveries.

- Transparency: A tracking number is no longer enough. The customer wants "Uber tracking" – to see the show live on the map and know the time window down to the minute.

- Flexibility: The customer wants to redirect delivery via app, change time slots or have them delivered to alternative locations (packing stations, trunk).

- Sustainability: This point is often underestimated, but is gaining massively in importance. The customer demands transparency about the CO2 footprint (see Green Logistics).

These expectations are seeping directly from the B2C to the B2B sector. Today, a buyer in mechanical engineering expects the same transparency in his pallet delivery as in his private pizza order.

Big Players vs. SMEs: Who will Win the Race?

Neo-logistics poses existential questions for every logistics service provider (LSP), but the answers differ massively depending on the size of the company.

Large logistics service providers (e.g. DHL, Kuehne+Nagel, Maersk)

The "big players" are investment drivers. They pour billions into their own IT platforms, gigantic automation centers (robotics) and the development of global data networks.

- Opportunity: They can create their own ecosystems, control the entire chain from production to the last mile, and leverage enormous efficiency advantages through economies of scale in the use of AI. They define the standards.

- Risk: Their sheer size makes them potentially sluggish. They have to be careful not to be overtaken by agile, purely digital "FreightTech" start-ups (such as Flexport or Sennder) that operate without "legacy systems" (old IT, own truck fleets).

Small and medium-sized (SME) freight forwarders

The pressure is highest for the classic medium-sized companies. They can't build their own AI departments or invest billions in robotics.

- Risk: If you don't digitize now, you will lose touch. If an SME freight forwarder still manages orders by fax or Excel, he is invisible to modern shippers who require an API connection. It will be degraded to an interchangeable "sub-carrier resource" for the major platforms.

- Opportunity: The niche! SMEs score points with flexibility, excellent customer service and specialization (e.g. pharmaceutical logistics, dangerous goods, white-glove service). Their survival strategy is cooperation. They have to dock onto the digital platforms (TMS providers, freight exchanges 2.0) and sell their niche expertise as a premium service.

Contract logistics company

For them, neo-logistics is the greatest opportunity. They are evolving from a pure "warehouse keeper" to a data-driven "supply chain orchestrator".

- Opportunity: By analyzing data from the WMS, IoT sensors in the warehouse and customer data (POS data of the retailer), they offer "value-added services": predictive replenishment (automatic reordering before the customer knows they need anything), co-packing, returns management 4.0 (quality inspection through AI image recognition) and even predictive maintenance for their customers' machines.

The New Power of Data: What's Changing for the Shipper

The shipper (the manufacturing industry, the trade) was the "client" for a long time. In neo-logistics, he becomes a "data partner".

In the past, the shipper's main demand was: "Price per pallet/container must decrease." Today, the demands are:

- Resilience: "Do you guarantee that my chain won't break?" The shipper requires multi-sourcing strategies, alternative routes and proactive risk management from their LSP.

- Transparency & Compliance: "Can you provide me with complete proof of where my raw material came from and that all standards were met?" The German Supply Chain Due Diligence Act (LkSG) is just the beginning here. The shipper needs to know what's happening in his chain and passes this pressure on to the logistics provider on a 1:1 basis.

- Data sovereignty: The shipper wants access to all data in real time (Estimated Time of Arrival - ETA). He wants to see the logistics data integrated into his own ERP system (e.g. SAP) in order to control his own production (just-in-sequence).

The relationship is changing from a transactional to a deeply integrated partnership. The LSP, which can only transport, loses. The LSP that can provide and interpret data wins.

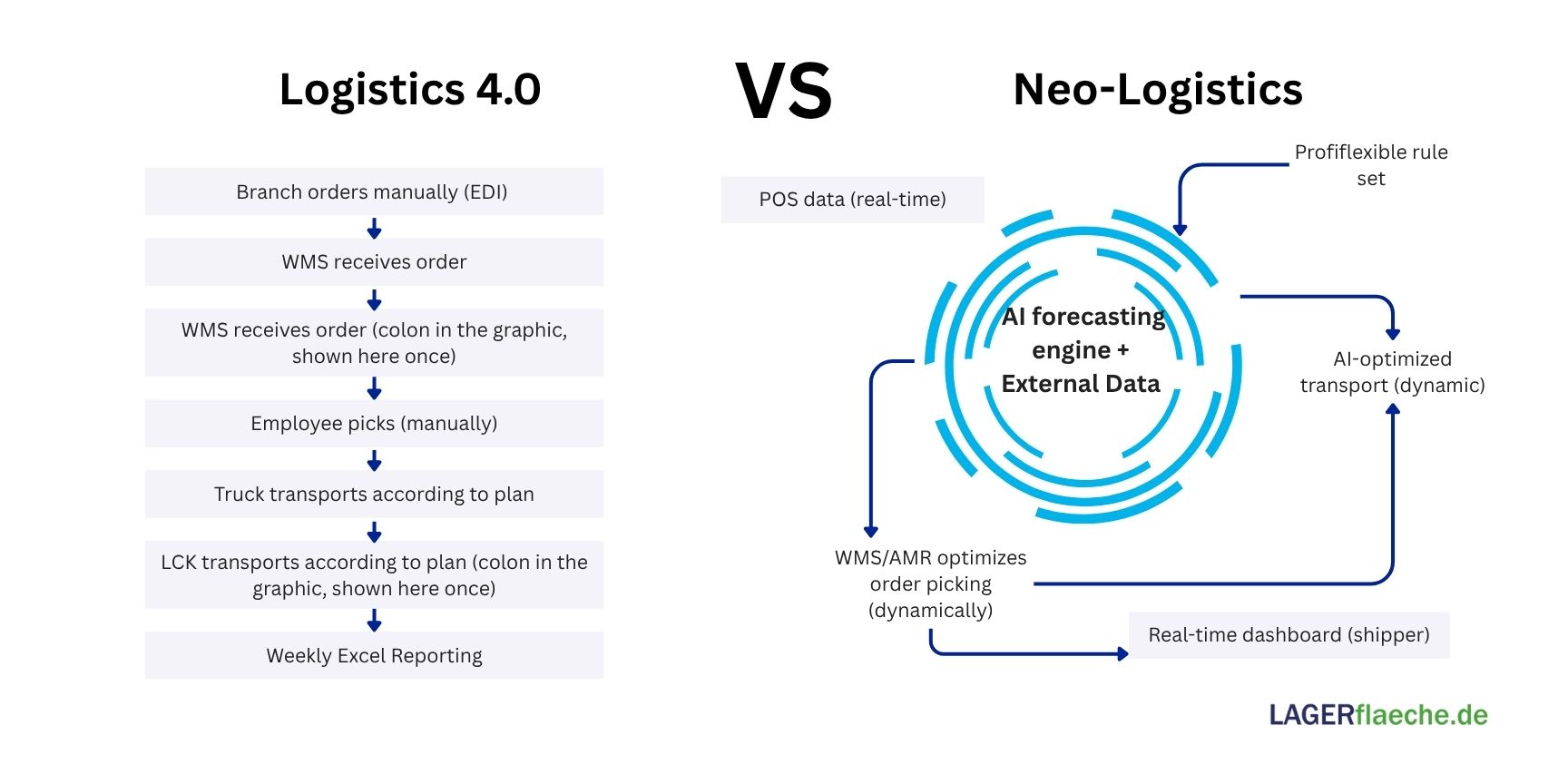

Practical Example: Contract Logistics Company "Müller & Partner" (hypothetical)

Let's take a medium-sized contract logistics company, "Müller & Partner", which operates a central warehouse for a medium-sized fashion retailer.

Situation (Logistics 4.0)

Müller & Partner uses a solid WMS. Orders from the retailer come via EDI, are picked (often still "man-to-goods") and distributed to the stores by truck. Reporting is done weekly via Excel.

Transformation (Neo-Logistics)

- Data exchange: Müller & Partner docks directly to the retailer's POS systems via API.

- AI use: An AI layer on top of the WMS now analyzes sales data (POS) and external data (weather, local events, social media trends).

- The benefit: The AI predicts that "Red Jackets Size L" will be sold out in the Hamburg branch on Friday due to a cold spell.

- Autonomous reaction: Before the store reorders, the AI at Müller & Partner triggers the replenishment order (predictive replenishment). In the warehouse, AI optimizes order picking (e.g. use of AMRs – Autonomous Mobile Robots – for this peak) and bundles transport with other shipments.

- Transparency: The retailer can see in his dashboard not only that the jackets are on the way, but also why they were sent (AI forecast).

Result

Müller & Partner is no longer a warehouse keeper, but an integral partner for the retailer's sales growth. It has multiplied its value.

Green Logistics: From a Fig Leaf to a Tough Competitive Factor

For a long time, "Green Logistics" was a marketing topic. That is over. Neo-Logistics is imperative Green Logistics. Why?

- Regulatory (the compulsion): The LkSG in Germany and the upcoming EU regulation (e.g. EU emissions trading ETS 2 for transport from 2027) make CO2 emissions a hard cost factor. Companies that do not measure and reduce their emissions become unprofitable or delinquent.

- Customer expectation (The Pull): As mentioned above, consumers demand sustainable options. Large shippers (e.g. IKEA, VW, Unilever) set themselves "Net Zero" targets and require all their logistics partners to do so by means of a declaration of commitment . Anyone who cannot provide a CO2 report will be kicked out of the tender.

- Efficiency (The Opportunity): Neo-Logistics and Green Logistics are mutually dependent. An AI-optimized route (neo-logistics) not only saves time, but also fuel (green logistics). An empty kilometre avoided by AI (platform economy) is the most efficient form of CO2 reduction.

The ability to precisely calculate emissions at shipment level (carbon tracking) and reduce them through alternative fuels (HVO, electric trucks, hydrogen) or offsetting is becoming a core competency.

Global Competition: Why Germany's Logistics Industry needs to Wake Up

The logistics are global. But the speed of transformation varies greatly around the world.

Germany

Germany is traditionally the logistics world champion (or at least runner-up). The World Bank's Logistics Performance Index (LPI) of 2023 sees Germany in the top group (3rd place, tied with several countries), but Singapore (1st place) and Finland (2nd place) show where the journey is heading: maximum digitization and efficiency.

- Strengths: Excellent infrastructure, high quality, strong SMEs (the "Mittelstand"), engineering skills (automation technology).

- Weaknesses: High wage and energy costs, bureaucracy, sometimes hesitant digitization among SMEs, acute shortage of skilled workers (esp. drivers, but also IT specialists).

Comparison China

China is betting on speed and economies of scale, driven by giants such as Alibaba (Cainiao) and JD.com.

- Difference: The state is massively pushing ahead with digitization (e.g. "Logink", a national logistics data platform). The integration of e-commerce, payment (Alipay) and logistics is a world leader. Investments in infrastructure (New Silk Road, automated ports such as Yangshan) are gigantic. The focus is less on data protection and more on datause.

Comparison USA

The USA is a market of extremes, dominated by tech giants.

- The difference is that innovation here is driven by the capital market and "Big Tech". Amazon (with its own sea, air, and land fleet) sets the benchmarks. At the same time, start-ups in Silicon Valley are driving innovation in autonomous driving (trucks, e.g. Aurora, TuSimple) and AI-based platform logistics (e.g. Flexport).

Conclusion of the comparison

While Germany is trying to digitize its established, high-quality processes, China and the U.S. are often building completely new, data-centric logistics ecosystems on greenfield sites. Germany's SMEs run the risk of being crushed between these giants if they do not specialize and network.

Conclusion and Outlook: Logistics is Dead – Long Live Neo-Logistics

The future of logistics is data-driven, autonomous and green. There will be no "business as usual".

- For logistics service providers (SMEs & large): It is not an IT project, it is a new business model. If you only sell cargo space, you lose. Those who offer data-based solutions, transparency and sustainability win. SMEs have to think in terms of niches and cooperations (platforms).

- For shippers: Logistics is becoming a strategic partner rather than a cost factor. In the future, the selection of the LSP will depend more on its API interface and CO2 reporting than on the pure freight price.

- For all of us: Neo-logistics is the decisive lever for making global flows of goods more resilient and sustainable.

The challenge is daunting, but the opportunity is greater: Logistics is reinventing itself – from a reactive "transport industry" to the proactive, AI-driven nervous system of the global economy.

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Live Cargo: Logistics, Collection Points and Value-added Services for Animal Transport

You can't store animals on pallets—so how does the supply chain for live cargo actually work? Discover the strict laws, Value Added Services, and specialized logistics hubs of animal transport in our comprehensive international overview....

CSRD-compliant: What tenants (must) demand from their logistics property now

Is your warehouse becoming an ESG black box? Discover our tenant checklist and learn exactly which data you must demand from your landlord for your CSRD reporting right now....

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....