Flex warehousing: The agile answer to fluctuating order books and uncertain markets

Table of Contents

- The Crisis of the Rigid Camp: Why Traditional Models Are Reaching Their Limits

- What is flex warehousing? The three core models in detail

- For which companies is the switch worthwhile?

- Practical example: The medium-sized online retailer

- The devil in the details: Contractual peculiarities in flex warehousing

- Globaler Check: Flex-Warehousing in Deutschland vs. International

- Why the world is stored differently: The reasons for the divergence

- Conclusion: Is flex warehousing the future or a niche?

Global supply chains are out of sync. The pandemic was followed by geopolitical tensions, energy price crises and inflation that makes demand patterns unpredictable. The traditional model of logistics – characterized by 5- to 10-year leases for warehouse space – is increasingly proving to be a rigid block on the leg in this environment. Companies that complained about a lack of storage space yesterday may be faced with half-empty halls today and still pay the full rent.

This instability is not a temporary disruption; it is the new normal. A study by McKinsey shows that companies today face a major supply chain disruption every 3.7 years, costing a month's worth of revenue (source: McKinsey, "Resilience for a volatile world", 2021). So how can companies manage their supply chain costs while remaining agile enough to respond to the next unforeseen spike – or valley?

The answer lies in making the physical infrastructure more flexible. Flex warehousing is more than just a buzzword; it has become a strategic necessity. But what exactly is behind it and for whom is it the right solution?

The Crisis of the Rigid Camp: Why Traditional Models Are Reaching Their Limits

Traditional storage contracts (often referred to as "commercial leases") are designed for stability and predictability. They offer the landlord security through long terms (often 5, 7 or 10 years) and the tenant a fixed, calculable cost block.

In a volatile market, however, these advantages are reversed:

- Overcapacity (risk of stranded assets): If demand falls, the rented space becomes a cost trap. Capital is tied up in unused space.

- Undercapacity (risk of "lost sales"): In the event of sudden peaks in demand (e.g. seasonal business, panic buying), the buffer is missing. The result: supply bottlenecks, dissatisfied customers and lost sales.

- Geographical commitment: A 10-year contract in Hamburg is useless if the customer base unexpectedly shifts to southern Germany or a new port (e.g. in the Benelux) becomes strategically important.

The rigid drafting of contracts prevents the necessary entrepreneurial agility. The need for flexible, needs-based solutions is obvious.

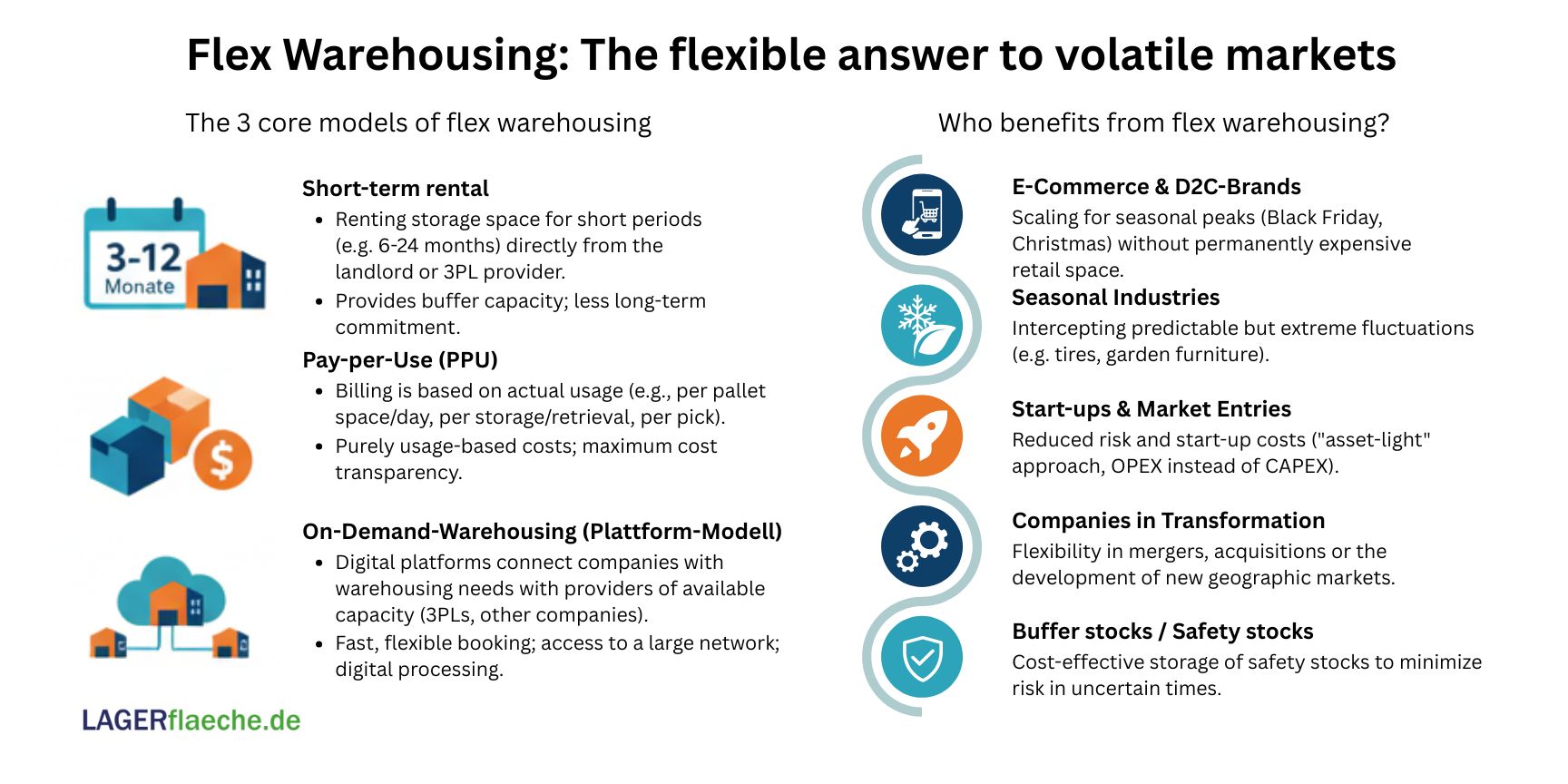

What is flex warehousing? The three core models in detail

Flex warehousing is not a single product, but an umbrella term for various approaches to using warehouse space and services as needed. Instead of area (square meters), service (pallet space, picking process) is purchased.

The three most common models are:

Short-term leases

This is the most traditional form of flexibilization. Instead of 5 years, you rent storage space for 6, 12 or 24 months. This is often a direct agreement with a property owner or a third-party logistics (3PL) provider. It provides a buffer, but is still area-based and less granular than the following models.

Pay-per-Use (PPU)

Here we enter the "cloud computing" model of logistics. Companies do not pay for a fixed space, but for the service actually used. Typical billing units are:

- Per pallet space (per day or week)

- Per stored and retrieved item (inbound/outbound)

- Per pick (picking process)

- Per parcel shipped

This model is almost exclusively offered by 3PL service providers, as it requires sophisticated warehouse management software (WMS/WMS) to accurately record performance.

On-demand warehousing (platform model)

This is the most disruptive form. On-demand warehousing providers (such as Flexe, Stowga or in Germany e.g. Everstox) do not operate any warehouses themselves. They are digital platforms – the "Airbnb of logistics".

They connect companies with storage needs (demanders) with companies that have free storage capacities and resources (suppliers). These can be 3PLs, but also manufacturing companies or retailers with seasonally unused space. Booking is often done digitally via a portal, with standardized processes and prices. The global market for on-demand warehousing is expected to grow at a compound annual growth rate (CAGR) of over 12% through 2027, according to Research and Markets (source: Research and Markets, "On-Demand Warehousing Market Report 2022").

For which companies is the switch worthwhile?

Flex warehousing is not the one-size-fits-all solution for everyone. A manufacturing company with extremely stable, high capacity utilization and special requirements (e.g. hazardous goods, pharmaceutical refrigeration) will probably continue to rely on its own or long-term leased distribution center.

However, Flex models shine in specific scenarios:

- E-commerce and D2C brands: No sector is more volatile. The need for storage space can triple or quadruple around Black Friday or the holiday shopping season. Flex warehousing allows you to scale for these peaks without paying for empty space throughout the year.

- Seasonal industries: Whether it's garden furniture in spring, ripening in autumn or chocolate before Easter – PPU models absorb these predictable but extreme fluctuations.

- Start-ups and market entry: Young companies cannot (or do not want to) tie up capital in long-term leases. An "asset-light" approach with on-demand storage reduces risk and start-up costs (CAPEX becomes OPEX).

- Companies in transformation: In mergers, acquisitions or the development of new geographical markets, flex warehousing offers the opportunity to test the market before committing to it for the long term.

- Buffer stock: In response to the supply chain disruptions, many companies have rethought their "just-in-time" strategies and are holding more safety stocks again. These buffers have to be stored somewhere – flexible renting is often cheaper than expanding the central warehouse.

Practical example: The medium-sized online retailer

Let's take "Genusswelt GmbH", a fictitious online retailer for specialties (wine, cheese, delicatessen). The company operates a central warehouse with 5,000 m² on the basis of a 7-year contract.

The problem: The Christmas business (Oct. - Dec.) accounts for 40% of annual sales. The gift baskets and wine orders exceed the capacity of the main warehouse. In the past, aisles were blocked, which drastically reduced efficiency (pick rates) and led to errors. Renting another hall for 5 years was too risky for the CFO.

The solution (flex warehousing): Genusswelt GmbH uses an on-demand provider. It books 800 pallet spaces for 12 weeks (mid-October to mid-January) with a 3PL service provider that has reported free capacity 30 km away.

The model: Billing is based on "pay-per-use". The systems (ERP of the dealer to the WMS of the 3PL) are connected via a standardized API of the platform.

The result:

- Cost control: Genusswelt GmbH only pays for the seats used during the peak season. From February to September, these costs are not incurred.

- Scalability: Next year, the booking can be adjusted to 700 or 1,000 seats, depending on the forecast.

- Efficiency: The main bearing remains efficient because it is not "delivered". The 3PL professionally handles the overflow volume.

The devil in the details: Contractual peculiarities in flex warehousing

Anyone who switches from a 10-year lease to a pay-per-use model is entering new legal territory. The biggest difference: We are moving from tenancy law (focus on the area) to service or work contract law (focus on the result).

This postponement has a massive impact on the drafting of contracts:

- Service Level Agreements (SLAs) are crucial: While a lease agreement regulates the "condition of the leased property", a flex contract regulates the "quality of the service". What must be in the contract?

- Inbound times: How quickly does the goods have to be received and booked in the WMS after arrival (e.g. "within 4 hours")?

- Pick accuracy: What error rate is tolerated (e.g. 99.8%)?

- Cut-off times: By when do orders have to be received to be shipped on the same day?

- Liability: In the case of a pure rental agreement, the tenant is often liable for damage to his goods (except in the case of gross negligence on the part of the landlord). In the PPU or on-demand (service) model, liability for the goods during storage and picking is transferred to the service provider. The liability limits (often per kilo or per claim, similar to the ADSp in Germany) must be clearly defined and covered by insurance.

- IT integration and data sovereignty: The contract must regulate who owns the data. Who pays for the connection of the systems (API setup)? What happens to the order data after the end of the contract (GDPR/GDPR compliance)?

- Flexibility of termination: This is the core. Instead of years of notice, notice periods must often be possible on a monthly or even weekly basis.

- Price escalation clauses: In a 5-year contract, there are often index adjustments. In a PPU model, which is heavily dependent on labor and energy costs, shorter-term price adjustments (e.g., diesel or energy floaters) are common. These must be transparent and comprehensible.

Global Check: Flex-Warehousing in Deutschland vs. International

The adaptation of flex warehousing varies considerably worldwide. Cultural, legal and economic framework conditions create a diverse picture.

Germany: The cautious optimizer

Germany is a country of engineers and stable medium-sized companies. "Ownership" (or at least long-term control) of assets is highly valued.

- Status quo: The German logistics real estate market is traditionally characterized by very long leases (5-10 years are the norm). The Fraunhofer Institute for Material Flow and Logistics (IML) confirms that the planning horizons in German SMEs are historically long.

- Flex adaptation: Flex models are primarily handled by established 3PL service providers who offer PPU models to their customers within their own long-term leased structures. Pure on-demand platforms (the "Airbnb model") have a harder time than in other markets, as trust in established partnerships is high.

- Legal hurdles: German labor law (strong protection against dismissal, temporary employment regulations) makes it difficult for warehouse operators to scale the workforce as flexibly as a pure PPU model would require. This drives up the cost of flexibility.

USA: The birthplace of on-demand

The US market is the most mature market for on-demand warehousing. Platforms like Flexe emerged here and raised hundreds of millions of dollars in venture capital.

- Driver: The sheer geographical size of the country. A retailer doesn't need one central warehouse, but a dozen to guarantee a 2-day delivery nationwide. The construction of such a network is much faster and less risky via flex warehousing (testing a market in Texas for 6 months).

- Labour market: A much more flexible labour market ("at-will employment" in many countries allows warehouse operators to quickly ramp up and down staff, which is the basis for PPU offers.

- E-commerce dominance: The immense pressure from Amazon is forcing other retailers to be agile. Flex warehousing is a means of competing for delivery speed.

United Kingdom (UK): Flexibility through crises

The UK market is also very mature, driven by two external shocks.

- Driver 1: E-commerce density: The British have one of the highest online shopping rates in Europe.

- Driver 2: Brexit: Brexit was a massive catalyst. The UK Warehousing Association (UKWA) reported a dramatic increase in demand for short-term warehouses (up to 25% in the quarters around the exit) as companies built up buffer stocks to avoid tariff delays (source: UKWA Reports, 2019-2021). This forced flexibility has changed the market permanently.

Asia (focus on China): Speed surpasses everything

In China, the logistics market is characterized by extreme speed and massive volume, dominated by giants such as Alibaba (Cainiao) and JD.com.

- Status quo: These giants operate huge, highly automated warehouses of their own.

- Flex Adaptation: Flex warehousing exists, but it's often part of the ecosystem of these major e-commerce platforms. Flexibility is achieved less by sharing "empty corners" than by the massive scalability of the technology and the connection of thousands of smaller courier services ("gig economy" approach to delivery).

Why the world is stored differently: The reasons for the divergence

Why is Germany adapting flex warehousing differently than the USA?

- Risk culture: German SMEs are often "asset-heavy" and rely on long-term control. US companies, which are more driven by the capital market, prefer "asset-light" models that protect the balance sheet (OPEX instead of CAPEX).

- Employment law: As mentioned, German protection against dismissal makes it difficult to flexibly scale personnel, which is necessary for PPU models.

- Contract law: German contracts are designed to last (tenancy law). U.S. contract law ("Freedom of Contract") is often more transactional and shorter-term oriented.

- Market structure: In Germany, established 3PLs dominate the flex market. In the USA, technology-driven platforms have been able to establish themselves as intermediaries (through VC capital).

Conclusion: Is flex warehousing the future or a niche?

Flex warehousing is no longer a niche solution, but it will not completely replace traditional long-term warehousing either. The future of logistics infrastructure is hybrid.

Successful companies will follow a "core-flex model":

- The "core": A strategically placed central warehouse (owned or rented on a long-term basis) for the background noise of the business, optimized for maximum efficiency.

- The "Flex Layer": An agile network of on-demand warehouses, PPU service providers and short-term rental space that covers seasonal peaks, promotions or new markets.

The instability of global markets is not a reason for resignation, but a call to innovation. Companies that learn to make their warehouse contracts and space as flexible as their production planning will be the winners of the "new normal". The decisive question for every logistics manager is therefore no longer whether, but how flex warehousing is integrated into their own network strategy.

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Live Cargo: Logistics, Collection Points and Value-added Services for Animal Transport

You can't store animals on pallets—so how does the supply chain for live cargo actually work? Discover the strict laws, Value Added Services, and specialized logistics hubs of animal transport in our comprehensive international overview....

CSRD-compliant: What tenants (must) demand from their logistics property now

Is your warehouse becoming an ESG black box? Discover our tenant checklist and learn exactly which data you must demand from your landlord for your CSRD reporting right now....

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....