The Architecture of Logistics: Who is Building the Future of the Supply Chain?

Table of Contents

- The Titans of the Area: Who are the Biggest Project Developers?

- David vs. Goliath: Advantages and Disadvantages of the Developer Greats

- The Duo Infernale: Interaction between project Developer and Construction Company

- Market Analysis 2026: Between Space Shortage and Yield Pressure

- Strategy Guide for Contract Logisticians and Warehouse Keepers

- Preserving Heritage: Refurbishment, Maintenance and ESG

- Global Comparison: Why Germany Ticks Differently

- Practical example: The Transformation of a 70s Warehouse

- Conclusion: Go from tenant to strategist

In recent years, the world of logistics real estate has changed from a "grey box on the outskirts of the city" to a highly complex investment property and critical infrastructure component. But while interest rates fluctuate and ESG (environmental, social, governance) criteria separate the wheat from the chaff, crucial questions arise:

- Who are the players dominating the market?

- What does the optimal interaction between developer and construction company look like?

- Which strategy saves the margin of contract logistics companies in volatile markets?

- Why is restructuring more complicated in Germany than in Poland or the USA?

In this deep dive, we analyze the mechanics behind the scenes of global and national project development.

The Titans of the Area: Who are the Biggest Project Developers?

The logistics real estate market is dominated by a handful of global giants and specialized national champions. According to current industry rankings (e.g. by Bulwiengesa or PropertyEU), the following players lead the field:

- Prologis: The undisputed world market leader. With over $200 billion in assets under management, they set the global standard for scalability and data management.

- Panattoni: The most active developer in Europe for years. Their focus is on aggressive expansion and the realization of large areas in record time.

- Goodman: An Australian heavyweight that focuses on high-end space in strategic gateway locations.

- SEGRO: Specialising in "light industrial" and urban logistics, particularly strong in the British and continental European markets.

Facts & Figures: In Europe alone, more than 20 million square meters of logistics space were completed in 2024 despite difficult financing conditions. Panattoni often held a market share of over 20% in new construction activities in Central and Eastern Europe (CEE).

David vs. Goliath: Advantages and Disadvantages of the Developer Greats

When should you choose a global player and when is the local "niche king" the better choice?

The big players (e.g. Prologis, Goodman)

- Advantages: High level of financial strength (financing security), worldwide network for customers (key accounts), standardization of hall types (efficiency), access to state-of-the-art PropTech solutions.

- Disadvantages: Often less flexible for individual special requests; The focus is usually on prime locations with correspondingly high rents.

The small/medium-sized developers (e.g. local family businesses)

- Advantages: In-depth knowledge of local building law and close contacts with municipalities (important for building permits), high flexibility for user-specific fit-outs (built-to-suit), more personal support.

- Disadvantages: Limited capital (higher risk of project delays), lower economies of scale when purchasing construction services.

The Duo Infernale: Interaction between project Developer and Construction Company

The relationship between a project developer and a construction company (general contractor, GC) is a symbiosis that often fluctuates between partnership and hard price management.

- The project developer: He is the director. He secures the property, clarifies the building law, acquires tenants and structures the financing. His risk is the market risk.

- The construction company (e.g. Goldbeck, Max Bögl): They are the craftsmen of logistics. Their focus is on execution reliability, adherence to deadlines and cost control.

Difference vs. cooperation: In the past, there was a strict separation. Today, the boundaries are blurred by design-and-build models. Large GCs like Goldbeck act almost like system suppliers. They offer standardised components that can reduce the construction time of a 50,000 m² hall to less than 9 months.

Critical success factor: The interface is risk management. Who bears the risk in the event of material price increases? In modern contracts, sliding clauses are often used in order not to jeopardize the cooperation due to insolvencies of the general contractor.

Market Analysis 2026: Between Space Shortage and Yield Pressure

The market for logistics real estate has changed fundamentally. While prime yields in prime locations such as Hamburg or Munich have risen slightly again (approx. 4.2% to 4.8%), supply remains the bottleneck.

- Vacancies in Germany' s top logistics regions, vacancy rates are often below 2.5%. This means that tenants have hardly any choice.

- Rental price development: Due to increased construction costs and ESG requirements, rents have risen by up to 15% in the last 24 months. Prime rents in Munich crack the €10.00/m² mark.

Question for the reader: Is a rent increase of 15% still sustainable for your logistics location while maintaining the same efficiency?

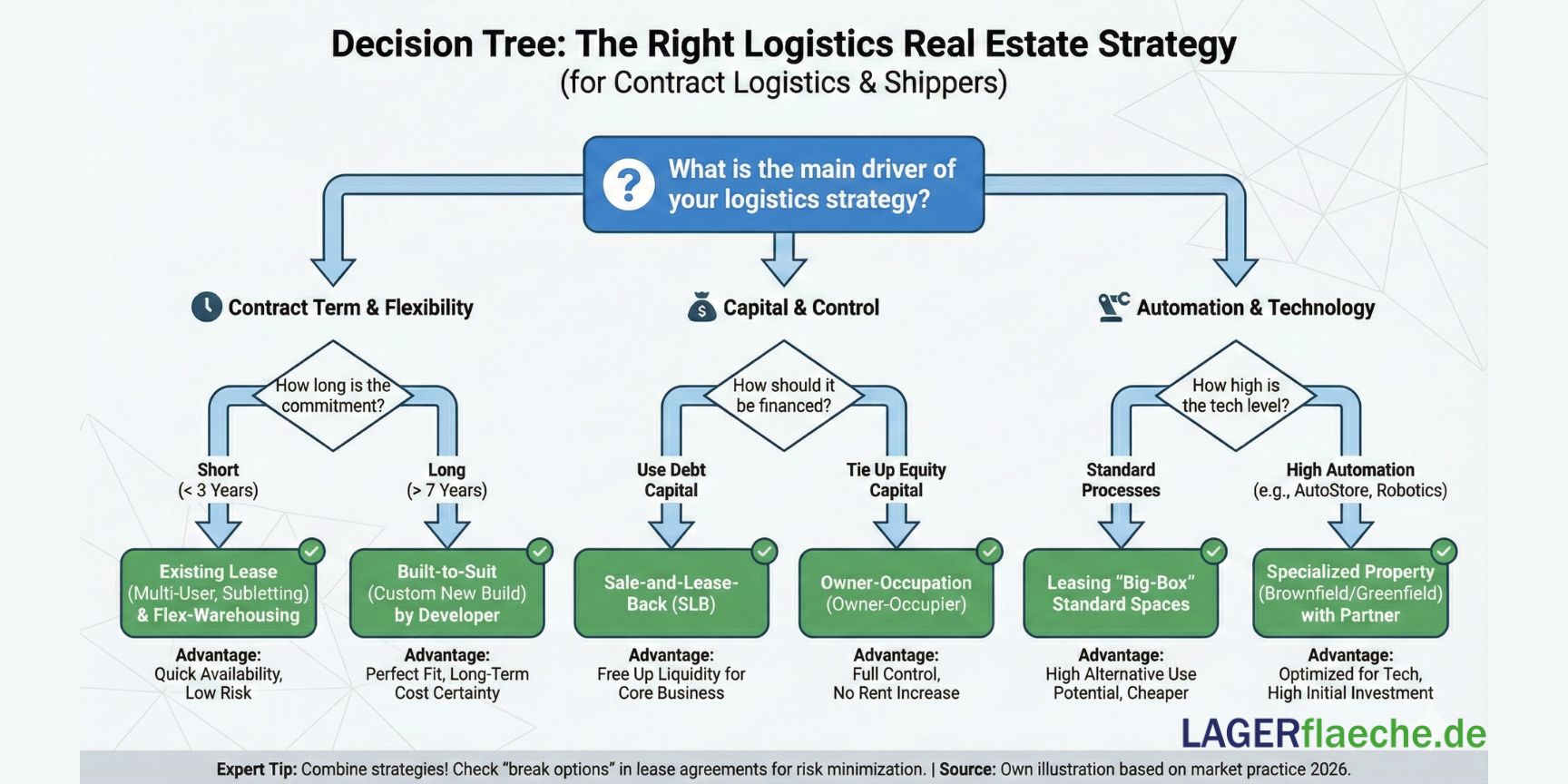

Strategy Guide for Contract Logisticians and Warehouse Keepers

Today, more than ever, a logistics service provider (LSP) has to think in terms of real estate strategy. Depending on the situation, a different approach is recommended:

| Situation | Recommended strategy | Contact person |

| Short-term new business (3 years) | Leasing of existing space (sub-letting) or multi-user halls. | Makler / Asset Manager |

| Long-term anchor contract (10+ years) | Built-to-suit by a developer. | Project Developer (Business Dev.) |

| High equity position | Owner-occupier. | Architect & General Contractor |

| Volatile Volumina | Use of on-demand logistics space (flex warehousing). | Tech Platforms / Logistics Aggregators |

Practical tip: Contract logistics companies should make sure that the term of the lease correlates with the term of the logistics contract. "Break options" are the most important negotiating tool.

Preserving Heritage: Refurbishment, Maintenance and ESG

The "Green Transition" does not stop at logistics. From 2026, properties without photovoltaics, heat pumps and LED control will become "stranded assets".

- Who is responsible?

- Maintenance: Usually the tenant (but often with the landlord – "Double/Triple Net" contracts).

- Refurbishment (revitalisation): The owner (asset manager).

- Contact: The asset manager is responsible for the long-term increase in value, while the property manager manages the day-to-day operations (repairs).

Focus on brownfield: Since green meadows (greenfields) are hardly ever approved in Germany, the future lies in the revitalization of old industrial wastelands. This is more complex (contaminated sites!), but ecologically and politically wanted.

Global Comparison: Why Germany Ticks Differently

The international comparison shows enormous differences in speed and costs:

Germany vs. Poland

- Poland: Approval procedures often take only 3-6 months. Labour costs are lower, and the availability of space is higher. Poland has become the "back-end" of German industry.

- Germany: Complex approval processes (12–24 months), strict species protection, high fire protection requirements. But: Greater location stability and better connections to end consumers.

USA & China

- USA: Focus on huge "mega-hubs" (100,000 m²+). REITs (Real Estate Investment Trusts) dominate here. The construction method is often simpler (concrete tilt walls).

- China: Extreme vertical logistics. In cities such as Shenzhen, five-storey logistics centres with ramp accesses for 40-tonne trucks are standard – a model that is becoming increasingly interesting for German metropolises (urban logistics).

Practical example: The Transformation of a 70s Warehouse

Scenario: A contract logistics company in the Ruhr area uses a hall built in 1978. The ceiling height is only 8 meters, the insulation is inadequate, and energy costs eat up the margin.

The solution: The project developer buys the site (sale-and-lease-back), demolishes the hall and builds a modern, 12-metre-high brownfield property with DGNB Gold certification.

- Result: 40% more pallet spaces on the same floor space, 60% lower energy costs thanks to PV system.

- Contact person for this: A specialist in brownfield development (e.g. Hagedorn or specialized teams at the big players).

Conclusion: Go from tenant to strategist

The logistics property is no longer a passive asset, but an active lever for competitiveness. Whether you scale globally with a giant like Prologis or occupy niches with a local partner depends on your long-term customer structure.

Important questions that you should clarify now:

- Are my current leases ESG-compliant or are there any additional payments?

- Do I have access to expansion areas at my core locations?

- Is my general contractor financially stable enough for the next major project?

Latest Blog Posts

Stay up to date with the newest trends, insights, and tips in warehouse and logistics. Our latest articles help you navigate the industry with confidence.

Live Cargo: Logistics, Collection Points and Value-added Services for Animal Transport

You can't store animals on pallets—so how does the supply chain for live cargo actually work? Discover the strict laws, Value Added Services, and specialized logistics hubs of animal transport in our comprehensive international overview....

CSRD-compliant: What tenants (must) demand from their logistics property now

Is your warehouse becoming an ESG black box? Discover our tenant checklist and learn exactly which data you must demand from your landlord for your CSRD reporting right now....

Cleaning in the Hall: From Chaotic Warehouse to High-gloss Logistics Center

From chaotic warehouses to high-tech hubs: Discover how AI cleaning robots, smart waste management, and strict industry standards are revolutionizing modern logistics while cutting costs....

with electronics and country-specific manuals.")

More than just transport: How value-added services are changing logistics forever

From simple transport to a true value-creation partner: Discover how integrated Value Added Services (VAS) like pre-assembly and quality control accelerate your supply chain and secure real competitive advantages....